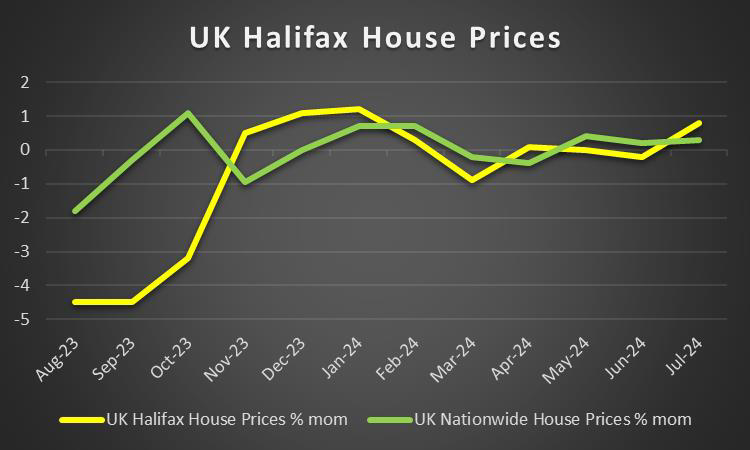

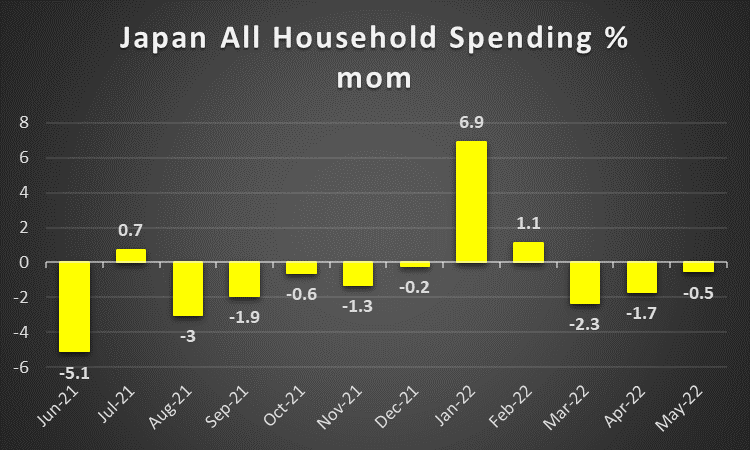

As we are nearing the end of the week, we have a look at what next week has in store for the markets. On the monetary front, we highlight the release from Canada of BoC’s interest rate decision on Wednesday. As for financial releases, we get Australia’s Building approvals for July, China’s Caixin Manufacturing PMI figure for August and Germany’s final manufacturing PMI figure for August. On Tuesday we get Australia’s current account balance for Q2, Switzerland’s and Turkey’s CPI rates, Canada’s manufacturing PMI and from the US the ISM manufacturing PMI figure, all being for August. On Wednesday, we get Australia’s GDP rates for Q2, Euro Zone’s final Composite PMI figure and UK’s Services PMI figure both being for August, Canada’s trade data, the US Factory orders and the JOLTS job openings figure, all being for July. On Thursday we make a start with Australia’s trade data for July, Germany’s industrial orders for the same month, the US ADP national employment figure for August and the ISM non-manufacturing PMI figure also for August. On Friday, we get Japan’s All household spending for July, Germany’s industrial output also for July, UK’s Halifax House prices for August, Eurozone’s revised GDP rate for Q2 and we highlight the release of the US employment report for August and simultaneously Canada’s employment data for the same month.

USD – The release of the US August employment report highlighted

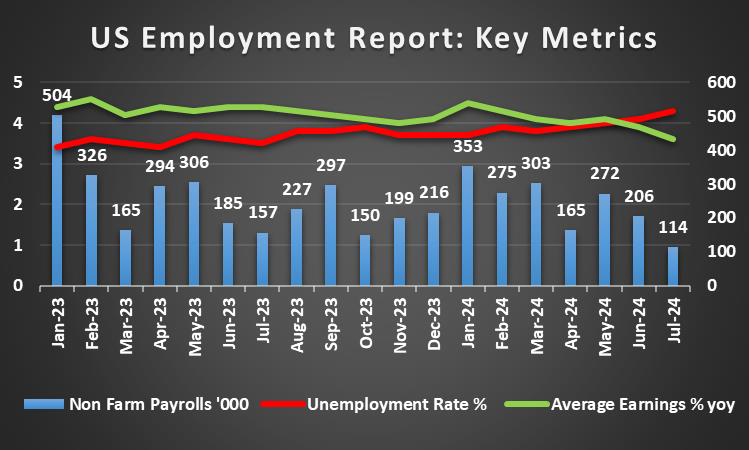

The USD was on the rise against its counterparts for the week and is about to interrupt a four week losing streak. We make a start by noting that as these lines are written, July’s US Core PCE rates are still to be released and could have a substantial impact on the greenback’s direction. On the monetary front we note that Fed Chairman Powell’s speech at the Jackson Hole Economic Symposium, sent some dovish signals enhancing the market’s expectations for extensive rate cuts by the Fed in the coming months. On a fundamental level, the preelection period is intense as the battle between Trump (R) and Harris (D) is ongoing, with the democratic candidate seemingly being able to widen the lead against Trump. Also we note the visit of US National Security Advisor Sullivan in China and a possible thawing of the tensions in the US-Sino relationships could cause the greenback to experience some safe haven outflows. On a macroeconomic level, we note that the revised GDP rate for Q2, accelerated if compared to the preliminary one. The release tended to enhance the Fed’s narrative for a possible soft landing and in turn may provide more confidence for the US economic outlook. In the coming week we highlight the release of the US employment report for August, with its Non-Farm Payrolls figure. The NFP figure is expected to rise from 114k in July to 163k and the unemployment rate to tick down to 4.2%. Should the actual rates and figures meet their respective forecasts, we may see the USD getting some support as the indicators would imply a possible tightening of the US employment market. Please note that Fed Chairman Powell in his speech at the Jackson Hole Economic Symposium, mentioned the shift in the bank’s attention from curbing inflationary pressures to the weakening US labour market, which in turn could enhance the impact of the release.

GBP – Fundamentals to lead the pound

The pound is about to end the week relatively unchanged if not slightly in the greens against the USD and seems to be also gaining ground against the EUR and JPY, in a sign of wider strength. For pound traders we note that on a fundamental level, Keir Starmer warned that his government’s October budget statement will be “painful” and asked the nation to accept “short-term pain for long-term good,” as reported by Bloomberg. The possibility of a tighter fiscal policy though failed to substantially weaken the pound. The markets seem to be trusting “no-drama” Starmer and are willing to tolerate some pain in UK fiscal policy for longer term profits, given also that the idea agrees with orthodox economics. At the same time the UK PM seems to be seeking a closer relationship between the UK and the EU and any improvement in the EU-UK relationships could prove to be beneficial for the pound on a fundamental level. On the monetary policy front we note that BoE Governor Bailey, stated at the Jackson Hole Symposium that inflation related risk is diminishing and is cautiously optimistic for the issue yet its too early to declare victory, as per the Financial Times. Overall the comments seem to be a prelude for further easing of monetary policy. For the time being the market seems to be pricing in a rate cut not in September, but in November and another one in December. On a macroeconomic level, there are no major financial releases in the coming week, hence we tend to expect fundamentals to provide direction for the pound.

JPY – Hawkish BoJ supports JPY

JPY seems about to end the week in the greens against the EUR yet loses ground against the USD and GBP. BoJ’s monetary policy may be the main driver behind JPY’s movement in the past few days. On the one hand the market’s expectations for another rate hike by BoJ seem to remain strong as it almost fully prices in, a rate hike in the September meeting and marginally another on in the December meeting. Please note that Bank of Japan Deputy Governor Ryozo Himino, expressed the bank’s readiness to raise interest rates should inflation remain at high levels. Please note that the nationwide July headline rate accelerated, while the acceleration of Tokyo’s CPI rates for August is also noted. Overall inflationary pressures seem to remain present in the Japanese economy that could justify further hikes by BoJ. On the other hand we note that JPY has reached sufficiently high levels against the USD and BoJ may prefer some FX stability for the Yen thus maintain rates at current levels. Should we see further indications that the Japanese central bank is about to hike rates in its coming meeting we may see the Yen gaining further ground. On the flip side, should carry trade be rejuvenated with the Yen on the short side, we may see JPY retreating. No major financial releases are on the calendar from Japan next week, hence we may see fundamentals to lead the way for JPY traders. Also let’s not forget JPY’s dual nature as a safe haven and a national currency and should we see a more risk averse market sentiment we may see JPY getting some support.

EUR – Eurozone’s revised GDP rate eyed

The EUR is losing ground for the week against the USD, the JPY and GBP, in a sign of wider weakness in the FX market. For the common currency, on the monetary front, we note the market’s expectations for the ECB to start cutting rates in its next meeting, in September and deliver another two rate cuts one in October and one in December. We note that ECB’s chief economist, Lane, stated that the bank expects wage growth to ease considerably in the coming year. The statement is practically enhancing the possibility of an easing of inflationary pressures in the Eurozone as wages is a key driver for inflation. On a monetary level we expect the common currency to continue to weaken as interest rate differentials may widen

between ECB refinancing rate and the rates of other major central banks. Even should other central banks cut rates according to the market’s expectations, the rates of the ECB are to be the lowest rates among major central banks, thus weighing on the EUR. On a macro level, we note that easing of inflationary pressures in the area, as the preliminary release for August, which tends to weigh on the EUR and may enhance the possibility for more rate cuts by the ECB. In the coming week, we highlight the release of Eurozone’s revised GDP rate for Q2 and a possible acceleration of the rate, could support the EUR as it would be easing the worries for a possible recession and vice versa. Also please note the release of Germany’s industrial output and orders for July, as an indication of economic activity for the crucial manufacturing sector of Germany. On a fundamental level, we highlight the elections in the German states of Thuringia and Saxony. The issue in the elections is that the far right party AfD, seems to be close to win or even passes the pole first. Should the AfD take the markets by surprise by strengthening substantially, we may see market worries for intensifying centrifuge forces in the EU being enhanced and thus weigh on the common currency.

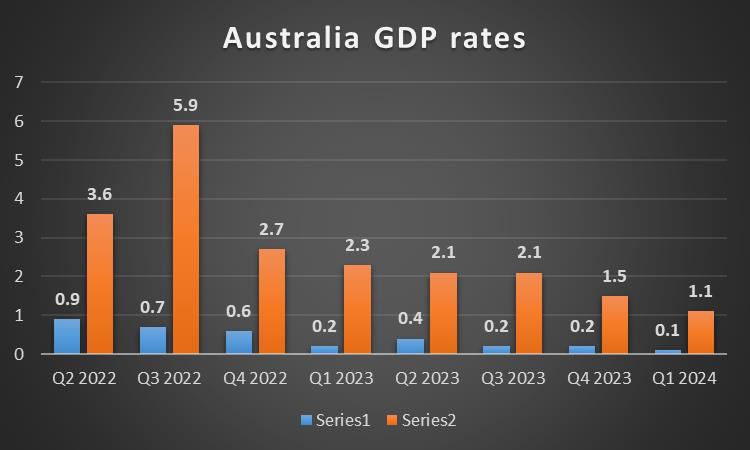

AUD – GDP rates for Q2 in focus

The Aussie is about to end the week in the greens against the USD. On a fundamental level for Aussie traders we note the possibility of an improvement of the US-Sino relationships, given the visit of US National Security Advisor Jake Sullivan in China. Discussions have been contacted about the Middle East and Ukraine, Taiwan and fentanyl. On the other hand the Chinese are expected to express disapproval over US tariffs on Chinese products and try to reaffirm their control over Taiwan. Should the negotiations fail to produce a positive outcome, market worries could intensify which could weigh on the Aussie given the close economic ties of Australia and China. From China we also note the release of the NBS and the Caixin manufacturing PMI figures for August. Should the indicators show that Chinese factories are still struggling to keep economic activity afloat, could weigh on the Aussie as another deeper contraction of economic activity in China could imply less exports of Australian raw materials to China. On a deeper fundamental level, we note the market’s perception for the Aussie as a riskier asset given its commodity currency nature. Should the market sentiment turn more risk averse we may see an adverse effect on the Aussie. On a macroeconomic level, we note the easing of inflationary pressures in the Australian economy for July. Yet the rates are still at high levels, which in turn may force RBA to maintain a tight monetary policy. Such a scenario could keep the Aussie supported on a monetary level, as RBA seems prepared to keep rates at high levels in a time that other central banks are easing or are considering easing their monetary policy by lowering rates.

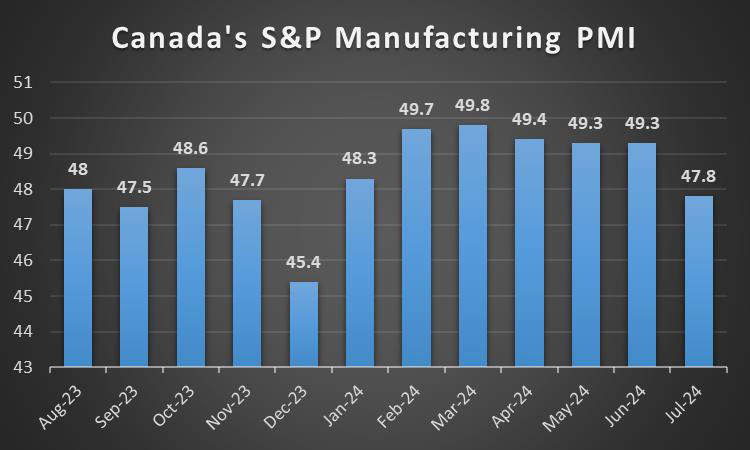

CAD – BoC’s interest rate decision in the epicenter

The CAD is about to end the week in the greens against the USD. We make a start for the Loonie with fundamentals, noting that the lockout of workers at Canadian railways came to an end rather early. On a deeper fundamental level, we note the wild swings of oil prices in the past week, given the status of the Canadian economy as a major oil producer. Fundamentals regarding the oil market tend to include the oil outage in Libya and the developments in the Israeli-Palestinian conflict. Should we see tensions in these two case rising we may see market worries for the supply chains of the international oil market intensifying and thus provide support for oil prices which could be overspilled towards supporting the Loonie as well. On a monetary level, we highlight the release of BoC’s interest rate decision next Wednesday. The market expects the bank to cut rates by 25 basis points and lower interest rates from 4.5% to 4.25%. It’s characteristic that currently CAD OIS, imply a probability of 97% for such a scenario to materialise. Yet the market is also expecting another two rate cuts in the October and December meetings. Given that a rate cut is allready almost fully priced in, should the bank cut rates as expected, it may keep the Loonie untouched and the market’s focus turn their attention towards the bank’s forward guidance. Should the bank signal its readiness to cut rates further in the coming meetings, we may see the Loonie losing ground, as the market’s dovish expectations may be verified partially.

General Comment

As a closing comment, we expect the USD to gain more of the initiative in the FX Market near the end of the week as the release of the US employment report for August will be nearing. As for US stockmarkets, we note that the earnings season is slowly calming down, easing the interest of the market participants for the US equities markets. The bullishness of US stockmarkets seems to have eased as we get mixed signals from major US stock market indexes. Also, NVIDIA’s earnings report despite showing improved and better than expected revenue and EPS figures, the company’s forward guidance tended to disappoint the markets. The release was reported having an adverse effect on the share’s price in the aftermarket hours. Should the markets in the coming week have a more cautious approach, we may see it having an adverse effect on US stockmarkets and vice versa. As for gold’s price we note that the negative correlation of the precious metal’s price with the USD remained somewhat blurred in the past few days. Despite a slight strengthening of the USD, mostly due to the acceleration of the US revised GDP rate for Q2, gold’s price failed to weaken substantially.

We also note the mixed signals sent by US yields that dropped for short term bonds such as the 2 year yet rose for longer term bonds like the 10 year. Overall we see signs of the negative correlation between the prementioned trading instruments slowly reviving, hence should we see the USD gaining some ground in the coming week, it could weigh on gold’s price.

如果您对本文有任何常规疑问或意见,请直接发送电子邮件至我们的研究团队,地址为 research_team@ironfx.com

免责声明:

本信息不被视为投资建议或投资推荐, 而是一种营销传播. IronFX 对本信息中引用或超链接的第三方提供的任何数据或信息概不负责.