US stock markets close distinctly lower

The tech sector suffered substantial losses, dragging Nasdaq and the S&P 500 lower. US economic data tend to be positive for US stock markets, and there was a relatively good start of the earnings season. Please note that market worries about possible overvaluations of tech shares are still present and could drag the sector even lower. Also, we note that Netflix posted higher than expected Q2 results, but its share price dropped as its forward guidance tended to disappoint.

USD about to end the week in the reds

The USD was relatively steady in the FX market during today’s Asian session, after yesterday’s gains. Nevertheless, the greenback is about to end the week in the reds as inflationary pressures in the US economy eased in the past month, both on a consumer and a producer’s level. Fed hike expectations seem to be easing, yet escalating tensions in the Iran-US conflict tend to keep oil prices high which in turn may reignite inflationary pressures in the US economy.

Oil market’s attention on the Middle East

Oil prices edged lower in today’s Asian session despite the US and Iran intensifying attacks against each other. The ceasefire has effectively been broken and oil flows from the Straits of Hormuz have been limited. The crisis is threatening to spill over to the Red Sea area as Iran has asked Houthis to also close the Straits of Bab al-Mandab. Substantial further escalation of tensions could boost oil prices further and vice versa.

Gold’s bearish tendencies remain

Gold is about to end its second week in the reds. Escalating tensions in the Middle East kept oil prices high, reigniting fears for inflationary pressures in the US economy. Such a development could force the Fed to keep its monetary policy tight. Given that the non-interest-bearing precious metal does not thrive in a high-interest-rate environment, gold’s price may suffer should market expectations remain hawkish for the Fed.

Other highlights for today

Today we get Euro Zone’s final HICP rates for June and from the US, June’s construction data and industrial production as well as July’s UoM consumer sentiment. In tomorrow’s Asian session, we get New Zealand’s trade data for June, UK’s Rightmove House prices for July, and from China PBoC’s interest rate decision.

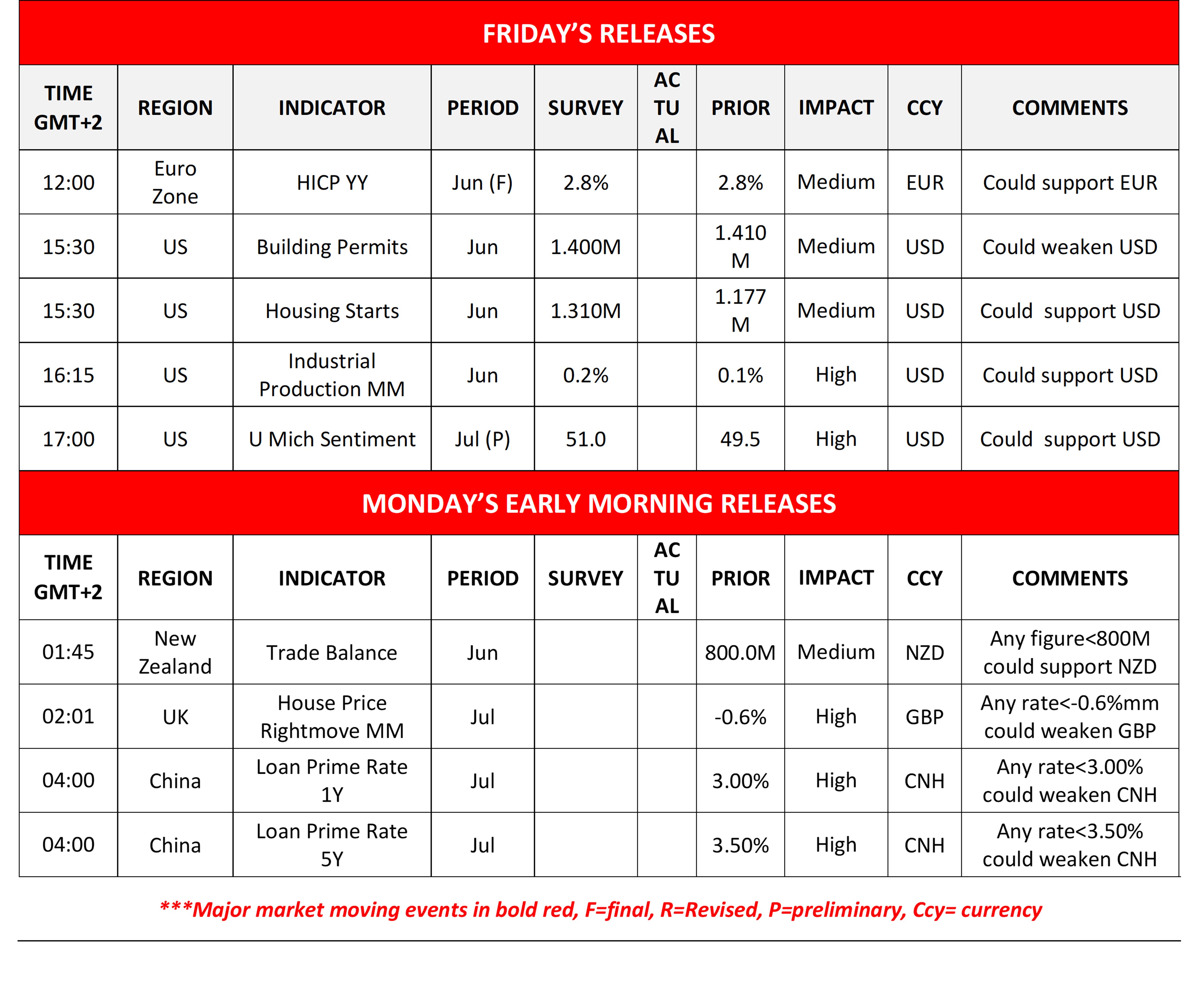

Charts to keep an eye out

Nasdaq dropped yesterday and during today’s Asian session, aiming for the 28200 (S1) support line. we note that the RSI indicator has dropped below the reading of 50, implying an intensifying bearish sentiment that could drag the index’s price action even lower. On the flip side, the index’s price action has hit on the lower Bollinger band which could slow down the bears. For a bearish outlook to emerge, we would require Nasdaq’s price action drop below the 28200 (S1) support line, thus opening the way for the 26870 (S2) support level. Should the bulls take over, we may see the index, rising breaking the 29675 (R1) resistance line and start aiming for the 30770 (R2) resistance level, marking an ATH for the index.

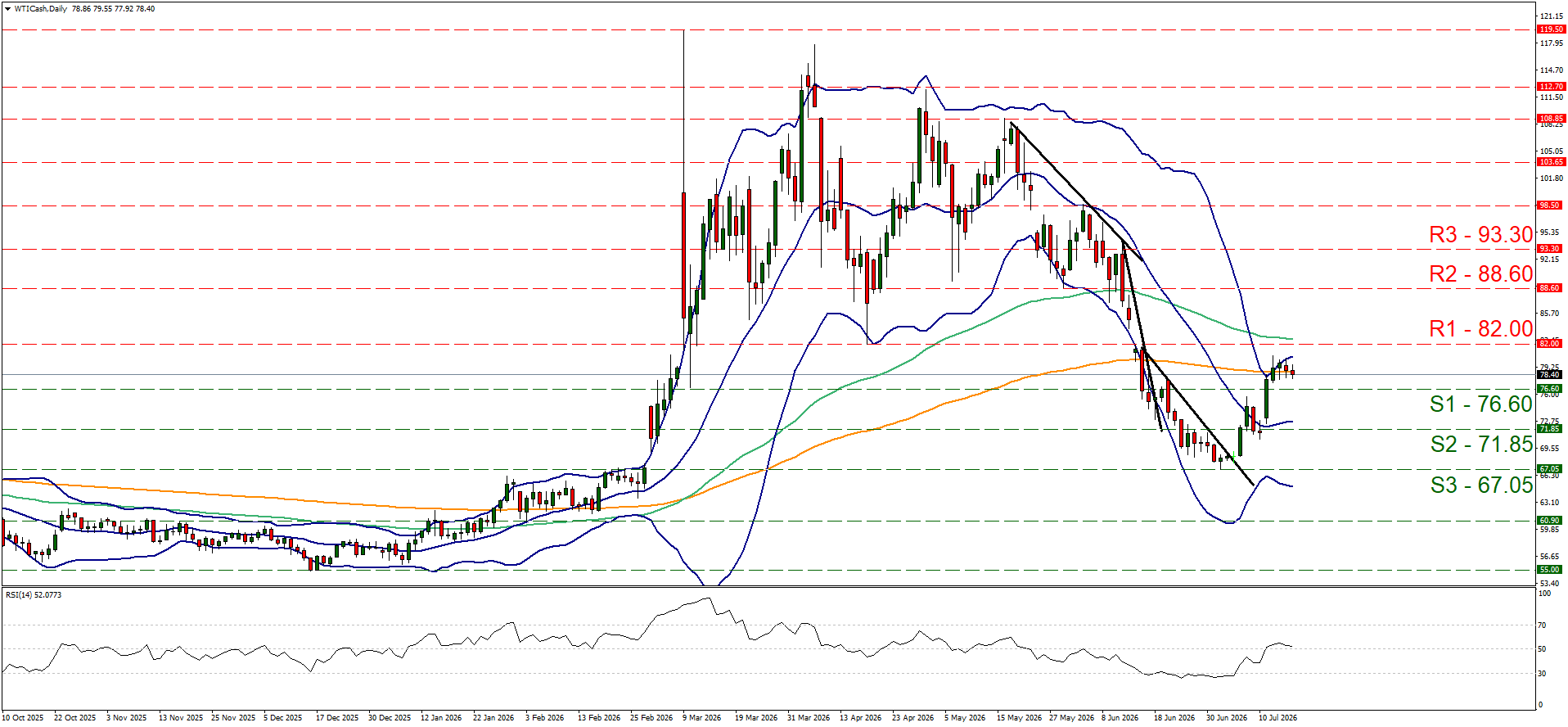

WTI’s edged lower, yet remained well between the 76.60 (S1) support line and the 82.00 (R1) resistance line. The RSI indicator continued to run along the reading of 50, implying the continuance of a rather neutral market sentiment, allowing us to maintain our bias for a sideways motion of the commodity’s price currently. Should the bulls regain control, we may see WTI’s price breaking the 82.00 (R1) resistance line with the next possible target for the bulls being set at the 88.60 (R2) resistance level. Should the bears get in the driver’s seat, we may see WTI’s price dropping, breaking the 76.60 (S1) support line, opening the gates for the 71.65 (S2) support level.

US 100 Cash Daily Chart

- Support: 28200 (S1), 26870 (S2), 25375 (S3)

- Resistance: 29675 (R1), 30770 (R2), 32500 (R3)

WTI Daily Chart

- Support: 76.60 (S1), 71.85 (S2), 67.05 (S3)

- Resistance: 82.00 (R1), 88.60 (R2), 93.30 (R3)

إخلاء المسؤولية:

لا تُعد هذه المعلومات نصيحة استثمارية أو توصية بالاستثمار، وإنما تُعد تواصلاً تسويقيًا. لا تتحمل IronFX أي مسؤولية عن أي بيانات أو معلومات مقدمة من أطراف ثالثة تم الإشارة إليها أو الارتباط بها في هذا التواصل.