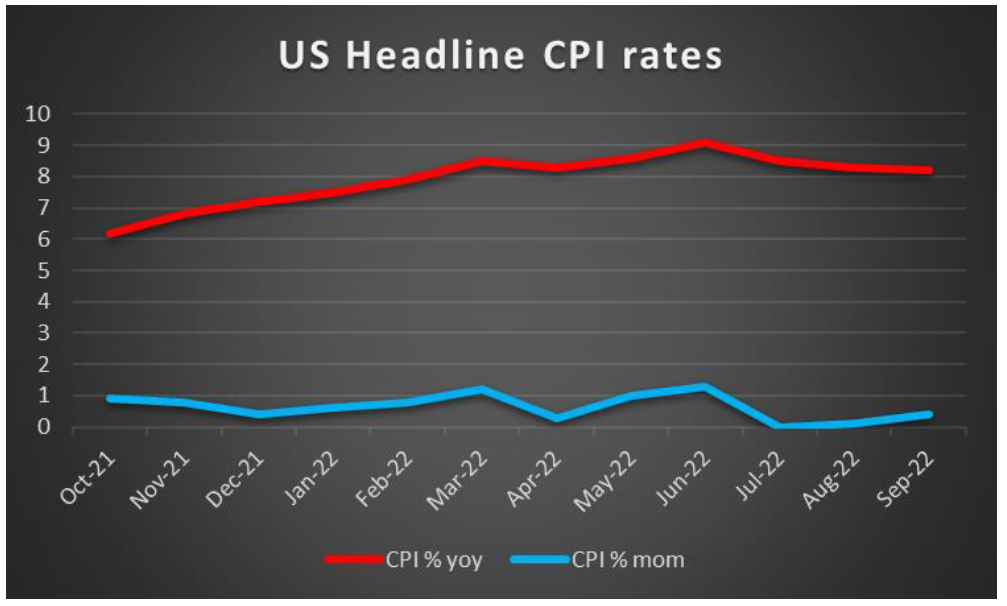

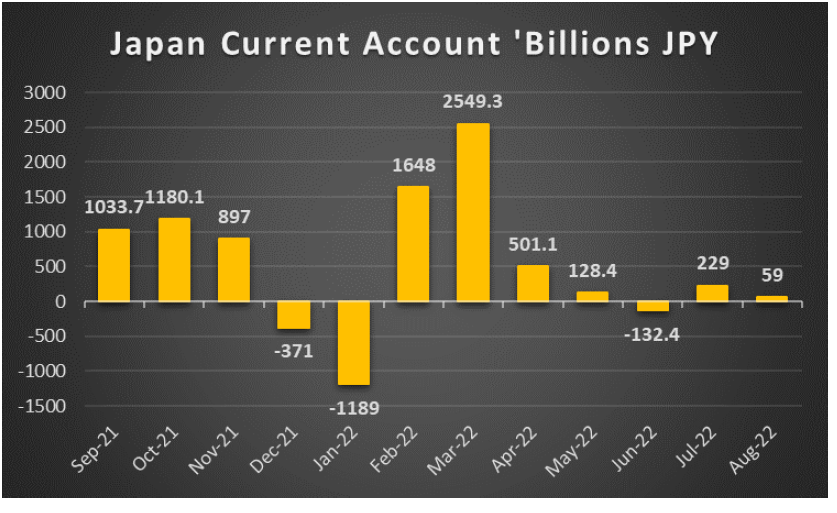

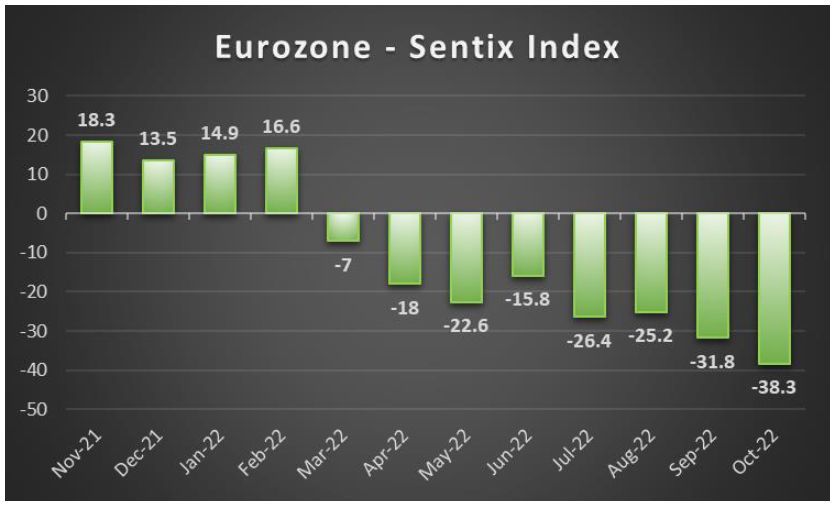

A rocky week is about to end, yet we note that the US employment report for October is still to be released and could stir substantial volatility in the markets. Next week is expected to be more quiet given that the number of high impact financial releases and monetary policy events is to be reduced substantially. Nevertheless, on the monetary front we expect monetary policymakers from various central banks to generate substantial interest among market participants and sway their opinion. As for financial releases, we make an early start on Monday with China’s trade data for October and continue with Germany’s industrial output growth rate for September, UK’s Halifax House prices for October and Eurozone’s forward looking Sentix index for November. On Tuesday, no release of high impact financial data is planned, while on Wednesday we get Japan’s current account balance for September and China’s inflation metrics for October. On Thursday we highlight the release of the US CPI rates for October while we also note the release of Norway’s and the Czech Republic’s inflation metrics for the same month as well as the US weekly initial jobless claims figure. Finally on Friday we note the release of Japan’s corporate goods price growth rate for October as well as Germany’s final HICP rate for the same month, UK’s preliminary GDP rates for Q3 and from the US the preliminary University of Michigan consumer sentiment for November.

USD – Midterm elections and CPI rates to move the markets

The USD is about to end the week higher against its counterparts, yet we note again that the release of the US employment report for October is still due out and could alter that. On a monetary level we note that the Fed as was widely expected hiked rates by 75 basis points yet failed to signal that it is ready to start slowing its interest rate hike path. Currently the market seems to be pricing in another 75 basis points rate hike in the December meeting and Fed Fund Futures show a 57.5% probability for such a scenario to materialise. We expect statements of Fed officials planned for the week to clarify further the bank’s intentions and depending on their content to move the USD. On a fundamental level we note the midterm elections that could shift the market’s opinion as well, as they may affect the US Government’s fiscal plans. For the time being the Democrats control both houses of Congress, the Senate and the House of Representatives, yet Republicans seem to be positioned to take control of the Senate. Such a scenario may leave the US with a split Government in other words, a Democrat President and a US Congress with a Republican veto. The issues which seem to be hot, albeit are not the only ones, are the economy and the high level of retail prices, abortion rights, immigration, Joe Biden’s presidency so far and its future and to a lesser degree education,

climate, public safety and gun control. Should the Republicans be able to take control over Congress, they may put the brakes on Joe Bidens’ extensive fiscal plans.

GBP – GDP rates eyed

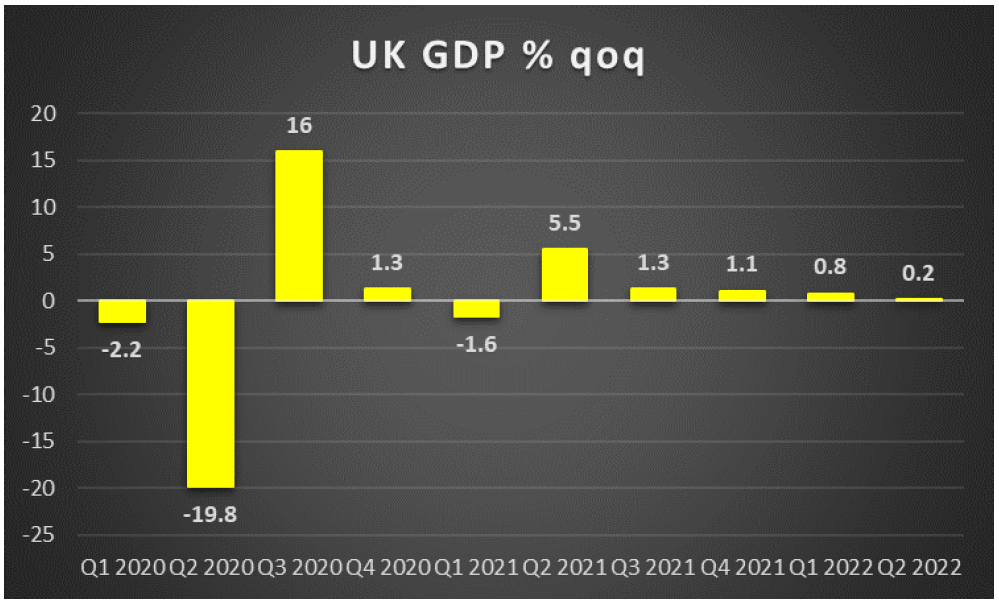

The pound is about to end the week lower against the USD, the EUR and the JPY in a sign of a broader weakness. On the monetary front BoE’s interest rate decision, verified the bank’s hawkish stance as it delivered a 75 basis points rate hike as was widely expected and reaffirmed its focus on curbing inflationary pressures in the UK economy. On the other hand it should be noted that the tightening of the bank’s monetary policy could have an adverse effect on the UK economic outlook as besides curbing inflationary pressures, it’s expected to also drag the UK economy in a deeper recession. The warnings and expectations of the bank and its Governor, for a deep and lasting recession were characteristic. Hence we would highlight the release of Q3’s GDP rate next Friday and should the rate show a contraction we may see the GBP weakening. On a fundamental level, the avoidance of political chaos seems to be the only good news for the UK economy. The new economic plan which its announcement was delayed for the 17th of November, may be also painful as austerity seems to be back on the menu. On a fiscal level the UK government has to cover a sizable void for the expenditure figure to meet income. The possibility of the UK government increasing borrowing seems to be a no-no for now given the high level of public debt. New taxes and reduced spending could be used for that aim, yet may also deepen the recession for the UK economy further.

JPY – First tweak to BoJ’s monetary policy in sight?

JPY seems about to end the week at the same levels it began again USD, yet gains widely against the EUR and the GBP. Still BoJ’s monetary policy is expected to play a key role in JPY’s direction. We note that in the minutes of the bank’s September meeting the sentiment tended to remain dovish in the grand scheme of things for BoJ, yet some worries for the depreciation of the Yen were present. We note the release of BoJ’s summary of opinions for October’s meeting on Tuesday, which could prove to be an interesting read. At the same time the rise of yields on an almost global level, tends to make it harder for BoJ to maintain its Yield Curve Control policy in place. BoJ Governor Kuroda’s hint on Wednesday, for a tweak to the ultra-low interest rates as a future option may not have been such a surprise afterall. Yet that may only be a way to blunten the criticism expressed, as he was reported stating to the Japanese Parliament that “For now, I don’t see the need to raise interest rates or make any modification to YCC,”. Overall we continue to see the banks’ dovish policy as being a drag for the Japanese currency and the fight of BoJ with the markets could intensify. On a fundamental level we note the missiles launched by North Korea on Wednesday and any further escalation of the situation could provide safe haven inflows for the Japanese currency, yet that does not seem to be one of the main market concerns for now.

EUR – Recession looms

EUR’s winning streak of two weeks against the USD is about to end. It should be noted that the common currency is also losing ground against JPY but not the pound. On a fundamental level the situation for Europe seems to be dire. Worries tended to heighten last weekend as Russia had announced that it would be pulling out of the Black Sea accord that allowed for the exports of Ukrainian grain. Since Wednesday Russia stated that it would re-enter the agreement, yet the tension and the worries were characteristic of the situation. Hence given the energy crisis, the confirmation of the contraction of economic activity and the high inflationary pressures the outlook for Eurozone’s economy is negative. Especially given that inflationary pressures accelerated for the month of October beyond market expectations reaching 10.7% yoy at a preliminary level. We should note at this point that on a monetary level, ECB President Lagarde stated on Tuesday that the bank’s mandate was price stability and that the bank should use all the tools available to deliver on that, also adding the bank’s determination to do what is necessary to bring inflation back down to its 2% target. Yet a further tightening of the bank’s monetary policy could deepen a possible recession for Eurozone’s economy, given the already existing slowdown of the GDP rate for Q3 at a preliminary level.

AUD – China’s trade data could move the Aussie

AUD is about to end the week near the same levels it begun against the USD. On a monetary level RBA’s interest rate decision to hike rates by 25 basis points was expected providing little volatility for the Aussie. In Governor Lowe’s statement it was mentioned that “A further increase in inflation is expected over the months ahead, with inflation now forecast to peak at around 8 per cent later this year” yet the time and sizing of the coming rate hikes is to be “determined by the incoming data”. It’s interesting that the bank had already started to ease its rate hiking path, despite still expecting inflation to peak at a higher level than the current one. However in a speech after the release of the bank’s interest rate decision, the Governor stated that the bank will not hesitate to hike rates at a faster pace if needed. For the time being the market seems to be pricing in another rate hike of 25 basis points in the December meeting with more to follow in 2023. Overall and at the current stage though, we still see the easing of the bank’s hawkishness weighing on the Aussie on a monetary policy level. On a more fundamental level, the Aussie as a commodity currency, tends to remain sensitive to the overall market sentiment, given that it’s considered to be a riskier asset. Should the market sentiment be more risk oriented we may see the Aussie gaining some ground, while should cautiousness characterize the markets we may see AUD retreating.

CAD- Fundamentals and oil prices to take over

Also the CAD seems about to end the week near the same levels it begun if not a bit weaker against the USD. It should be noted that also Canada’s employment data along with the US employment report for October, are still to be released and could alter that picture for the end of the week. On the monetary front it should be noted that BoC Governor Macklem was reported stating that inflation measures have stopped rising rapidly yet have still to drop substantially. It was characteristic that he reiterated that “this tightening phase will draw to a close. We are getting closer, but we are not there yet”. The statement tended to reaffirm the view that more rate hikes are necessary, yet at the same time may be of smaller size in the future which would underscore the change of tone of the bank, as expressed in its last interest rate decision. On a more fundamental level, we note that WTI prices are about to edge higher for a third week in a row and should that tendency continue we may see the Loonie getting some support as oil is one of the main export products of Canada. On the flip side, should worries for a possible recession intensify and weaken oil prices, as the commodity’s demand side could come under threat, we may see the Loonie relenting some ground. Also as a commodity currency CAD is considered to be more sensitive to the overall risk sentiment of the market and should a more risk oriented sentiment prevail we may see the CAD getting some support.

General Comment

In the coming week given that the number of high impact financial releases and monetary policy events are to lesser in number as mentioned before, we may see fundamentals playing an increased role for the markets. It should be noted that the USD may relent some of its initiative over other currencies, creating a more balanced environment for traders. Nevertheless, the US CPI rates are still to be released and could bring the greenback under the spotlight. At the same time we note that the earnings season for US stockmarkets is still on yet the number of high profile companies to release their reports is to be reduced, thus we may see some of the market’s interest shifting away from equities markets. Some exceptions like Disney on Tuesday, Ali Baba on Thursday and Burberry on Friday are still present though and could make headlines, turning the market’s attention. On a more fundamental level US yields seemed to be on the rise for the past few days and should that tendency be continued, we may see the USD getting some additional support, while gold prices could suffer. Overall, we tend to see the negative corelation of the precious metal with the USD and yields, resurfacing in the coming week, albeit we have to note that we tend to be somewhat disappointed from the lack of volatility for the precious metal’s price for the week. Please note though that gold’s price is currently trading near a two year low level which may make it harder for the bears to advance.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.