The USD edged lower yesterday after the release of the US PPI rates for October, slowed down more than expected, intensifying market expectations that inflationary pressures in the US economy have peaked and are slowing down. Hence the release also tended to solidify the markets’ expectations for the rate hiking path of the Fed to ease, while such expectations were further enhanced by Philadelphia Fed President Harker’s comment that the Fed may start considering pausing the rate hikes. On the other hand, we have to note that Atlanta Fed President Bostic stated in an essay that he does not see the Fed’s tighter monetary policy having dented inflation and foreshadowed more rate hikes to come. Yet we must note that the greenback got some safe haven inflows yesterday as a Russian made missile reportedly hit Poland, killing two persons. The fact that such a missile would hit the soil of a NATO member state and its possible consequences tended to intensify the market’s uncertainty and sense of urgency, yet we note comments made both by Polish and US officials, including President Biden, which downplayed the significance of the incident, thus we expect a calming of the markets.

Nevertheless, the issue had an adverse effect on US stockmarkets, which ended the day with mixed results, given also that the Q3 earnings reports of both Walmart and Home Depot were better than expected also implying a healthy demand appetite in the US economy. On the other hand, we cannot miss out on noticing that Vodafone missed its revenue target, by reaching only half the expectations of the market and for today we would note the release of the earnings reports for Baidu (#BIDU), Cisco (#CSCO), and Nvidia. Should a positive risk on sentiment be able to surface we may see US stockmarkets being clearly in the greens once again. Back in the FX market and across the pond we note that the common currency got some support initially yesterday, as data showed that pessimism for Germany has lightened up, and the situation on the ground is no longer as bad as it used to be in October. Across the Channel the release of the UK employment data on the other hand showed that despite a tick up of the unemployment rate it remains at relatively low levels, yet the fact that the employment change figure missed its target tended to create some worries for the UK economy’s ability to create new jobs.

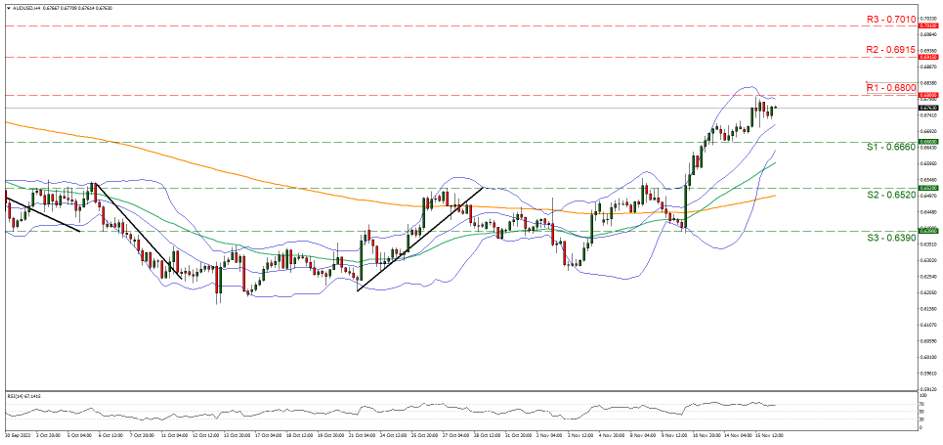

AUD/USD rose yesterday yet seems to find resistance at the 0.6800 (R1) level. Given that the pair was not able to break above the R1, we expect AUD bulls to calm down and the pair to maintain a sideways motion, yet the RSI indicator is running along the reading of 70 implying a rather bullish sentiment. Should the bulls be in charge, we may see AUD/USD breaking the 0.6800 (R1) line and aim for the 0.6915 (R2) level. Should the bears take over, we may see AUD/USD breaking the 0.6660 (S1) support line and aim for lower grounds.

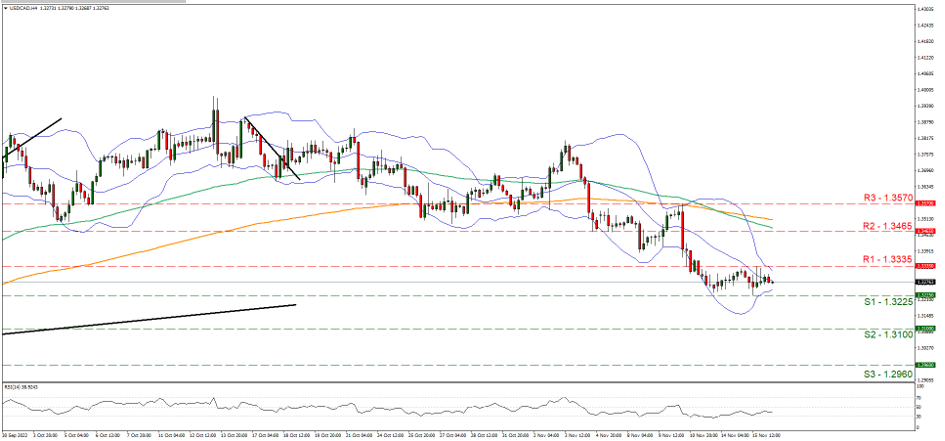

USD/CAD seems to maintain a rangebound movement between the 1.3255 (S1) and the 1.3335 (R1) levels. We tend to maintain a bias for the sideways motion to continue, yet are worried for the bears as the RSI indicator below our chart is below the reading of 50. Should a selling interest be expressed by the market we may see USD/CAD breaking the S1 and aim for the 1.3100 (S2) support level. Should the pair find fresh buying orders along its path we may see it breaking the R1 and take aim of the 1.3465 (R2) level.

Other highlights for the day:

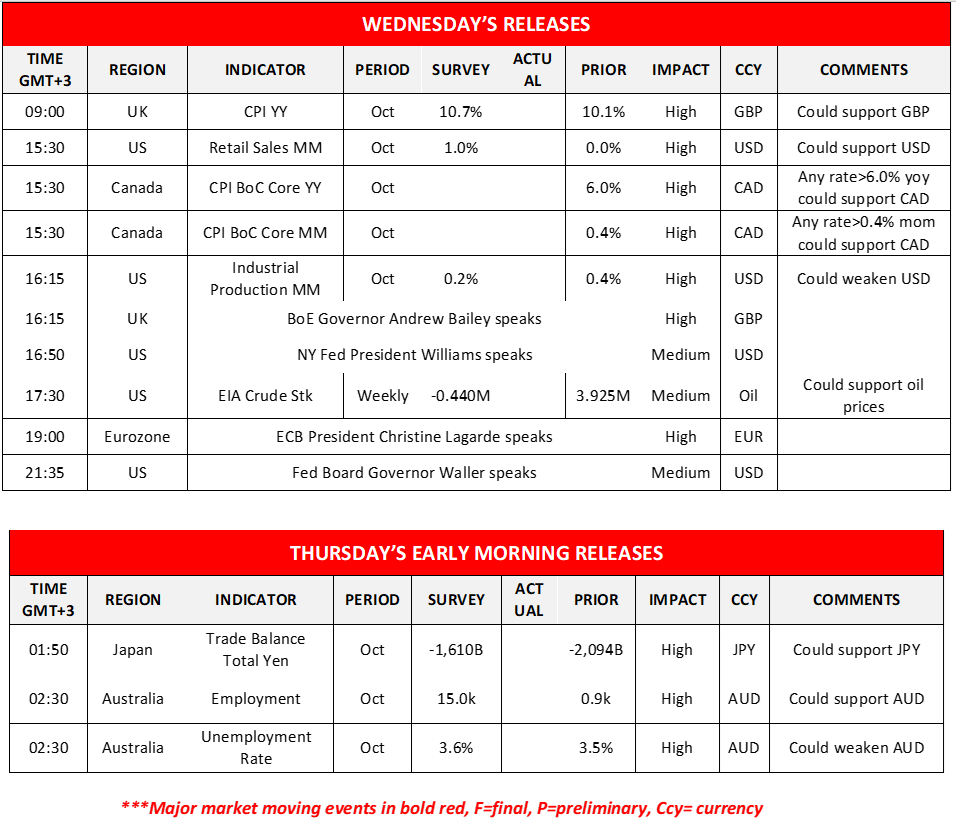

Today we note the release of UK’s CPI rates, the US retail sales and industrial production and also highlight Canada’s CPI rates with all metrics being for October. Oil traders on the other hand may be more interested in the release of the weekly US EIA crude oil inventories figure given also that API showed a substantial drawdown in last week’s US oil reserves yesterday. On the monetary front we note that BoE Governor Andrew Bailey, NY Fed President Williams, ECB President Christine Lagarde and Fed Board Governor Waller are scheduled to make statements. During tomorrow’s Asian session we note the release of Japan’s trade data and highlight the release of Australia’s employment data, both being for October.

USD/CAD H4 Chart

Support: 1.3225 (S1), 1.3100 (S2), 1.2960 (S3)

Resistance: 1.3335 (R1), 1.3465 (R2), 1.3570 (R3)

USD/JPY H4 Chart

Support: 0.6660 (S1), 0.6520 (S2), 0.6390 (S3)

Resistance: 0.6800 (R1), 0.6915 (R2), 0.7010 (R3)

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.