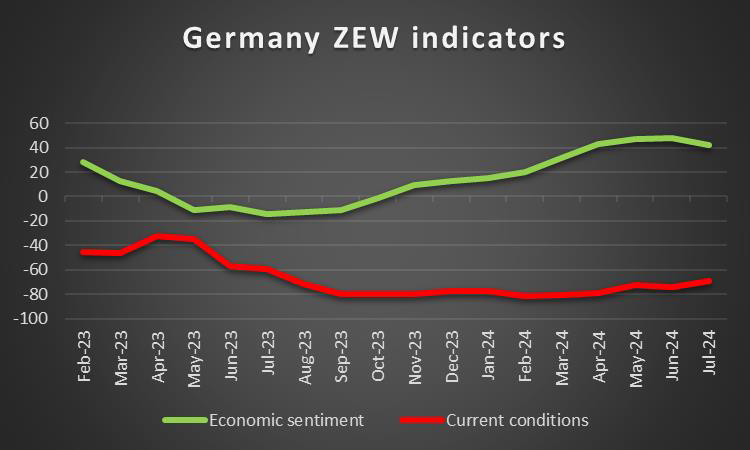

With the week coming to an end, we take a look what next week has in store for the markets. On a monetary level, we highlight the release of New Zealand’s interest rate decision on Tuesday and Norway’s interest rate decision on Thursday.As for financial releases we make a start on Monday with the release of the UK’s manufacturing output for June, followed by France’s CPI and the Czech Republic’s CPI rates for July. On Tuesday we get the UK’s unemployment rate for June, followed by Germany’s ZEW economic sentiment and current conditions figures for August, followed by the US PPI Machine manufacturing figure for July. On Wednesday we get Japan’s Reuters tankan-non manufacturing index figure , the UK’s CPI rates, Sweden’s CPI rates and France’s CPI rates all for July, followed by the Eurozone’s preliminary GDP rates for Q2 and the US CPI rates for July. On Thursday, we get Japan’s machinery orders rate for June, followed by Japan’s GDP rates for Q2, Australia’s unemployment data for July, China’s industrial output, retail sales rate and unemployment rate all for July, the UK’s preliminary GDP rates for Q2, the US NY Fed manufacturing figure and Philly Fed business index figures for August, the US Retail sales rate and Industrial production rate both for July. On Friday we get Canada’s housing starts figure and the US University of Michigan preliminary consumer sentiment figure for August.

USD – US CPI rates next week

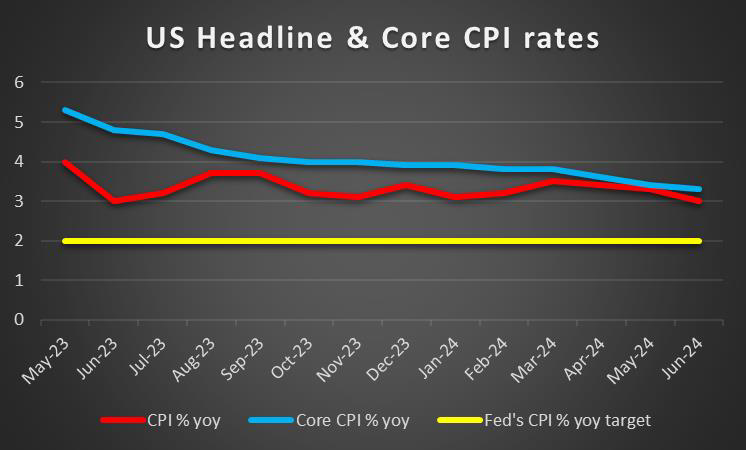

On a fundamental level for the USD we note that the US Presidential race remains tight with the two candidates set to debate on the 10th of September on ABC. On a macroeconomic level, we note the release of the US Employment data for July last Friday which caused a scare that the US labour market may not be as resilient as was expected, following the unemployment rate unexpectedly ticking upwards from 4.1% to 4.3%. The higher-than-expected unemployment rate intensified recession worries in the US economy, although an increase of 0.2% in our view did not warrant such an extreme reaction from market participants and thus although we remain concerned about the overall economic picture of the US economy, it is our view that the markets overreacted. Nonetheless, the economic jitters may have eased after Monday’s ISM Non-Manufacturing PMI figure came in as expected at 51.4 and thus managed to escape contraction territory. Moreover, the Atlanta Fed GDPNow preliminary GDP rate for Q3 came in higher than expected at 2.9% implying a greater than expected expansion of the US. On a monetary level, we note that there was talk about a potential emergency rate cut by the Fed next week, although followed the aforementioned financial releases, we tend to believe that it may not be necessary. Furthermore, San Francisco Fed President Daly stated on Tuesday that “it’s clear inflation is coming down closer to our target”, implying that the bank’s 2% inflation target is in sight and thus, the bank may be preparing to cut interest rates in the near-term, which in turn may weigh the greenback and alleviate some concerns about an overtightening scenario by the Fed.For next week, of interest may be the US CPI rates, which are expected to showcase easing inflationary pressures. Such a scenario may provide the Fed with greater confidence should they decide to cut rates in their September meeting.

GBP – GDP rates next week

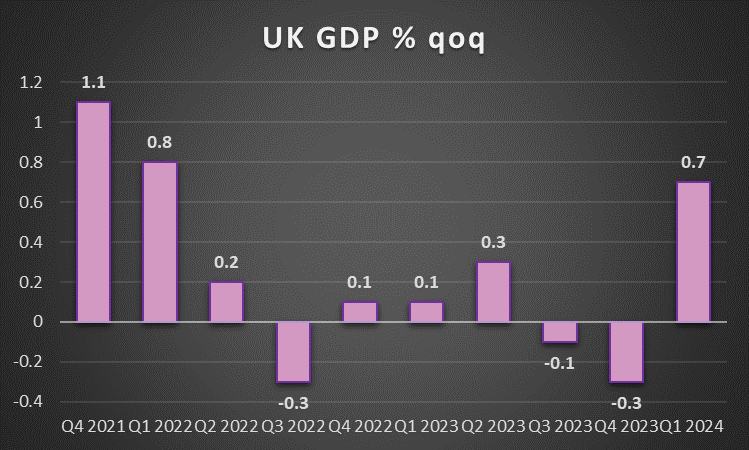

On a fundamental level, the UK’s political scene is looking shaky, with numerous riots taking place in the nation.On a macroeconomic level, we note the UK’s final composite and services PMI figures for July exceeded expectations, implying a greater than expected expansion of the UK economy from a services and general standpoint, which may have aided the pound. In addition, the UK’s construction PMI figure for July also exceeded expectations implying also an expansion in the construction sector of the economy, which also appeared in the Halifax house price index rate for July which also came in higher than expected at 0.8%. Overall, the financial releases stemming from the UK tend to point a positive picture and pound traders may be looking for that momentum to be carried into next week, where we are set to receive the UK’s CPI rates for July and preliminary GDP rates for Q2. In the event that the GDP rates come in higher than the prior rates, it may imply that UK economy is expanding and thus the economic situation in the UK could be improving. For the CPI rates, should they come in higher than expected, it may imply that inflationary pressures in the UK economy may have not subsided and thus could increase pressure on the bank to keep interest rates steady rather than continuing on their monetary policy easing cycle. Furthermore, should the CPI rates showcase an acceleration of inflationary pressures, the bank’s 25bp cut last week may be considered premature. On the flip side, should the CPI rates showcase easing inflationary pressures in the UK economy, it may validate the bank’s decision to but interest rates and may embolden them to continue on their current path. Overall, next week is set to be crucial for pound traders, as key financial releases are due.

JPY – BOJ hesitation after heightened market volatility

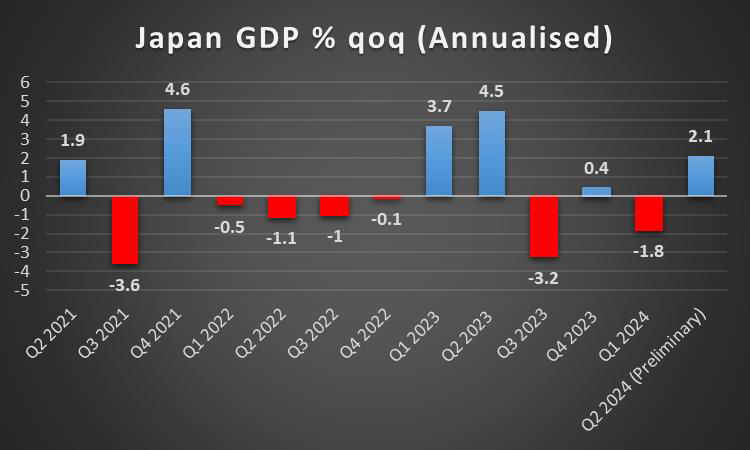

We continue to maintain our view that there may be more way to go to push the JPY higher, yet that remains to be seen. On a monetary level The BOJ’s summary of opinions for their July meeting was released earlier on this week. Within the statement, it appears that BOJ policymakers debated on whether or not to raise the monetary policy rate even further, having stated that “The current economic situation seems to be favorable enough that the Bank can raise the significantly low policy interest rate to some degree”. The mention that the interest rates are “significantly low” tends to imply a willingness by the bank to raise rates more aggressively, which in turn may aid the JPY. However, the recent developments in which the carry trade appears to be unwinding, in combination with some concerns about the ‘health’ of the global financial markets, may disrupt the BOJ’s ambitions. Moreover, in the SOP the neutral rate “seems to be at least around 1%”. Nonetheless, the overall document appears to have been hawkish in nature. On the other hand, BOJ deputy Governor Uchida during his remarks earlier on today downplayed the possibility of near-term hikes, with Reuters citing the Deputy Governor having said that “We won’t raise interest rates when financial markets are unstable”, implying that the recent market volatility is not favorable for the bank and thus appears to contradict the bank’s summary of opinions. For next week, we would take a look at Japan’s GDP rate for Q2 which is set to showcase an expansion of the Japanese economy and thus could further aid the JPY. On the flip side should it showcase a contraction it may have the opposite effect.

EUR – GDP rate for the zone next week

On a fundamental level for EUR traders we note that the EU’s artificial intelligence act is now officially enforceable since Thursday.On a monetary level, we note that ECB as was widely relatively quiet this week and as such we will focus more on the macroeconomics. As such we turn our attention to Germany’s and France’s respective Services and Composite PMI figures for July which were released alongside each other. Starting with France their composite and services PMI figures came in lower than expected, whereas the opposite occured for Germany who’s composite and services PMI figures exceeded expectations . As such attention may turn to the release off the Eurozone’s preliminary GDP rates for Q2 next week, in order to gain greater clarity of the economic situation in the zone as a whole. The current expectation for the preliminary GDP rate for Q2 on a qoq basis is 0.3% which would be identical to the prior quarters GDP rate of 0.3%, thus implying an expansion in the zone’s economy. Such a scenario may provide support for the EUR . On the flip side should the preliminary GDP rates showcase a contraction of economic activity in the Eurozone, it could instead weigh on the EUR. Moreover, of secondary interest may be Germany’s ZEW economic sentiment and current conditions figures for August which are due out on Tuesday, as a gauge of the consumer perspective of the Germany’s economic situation.

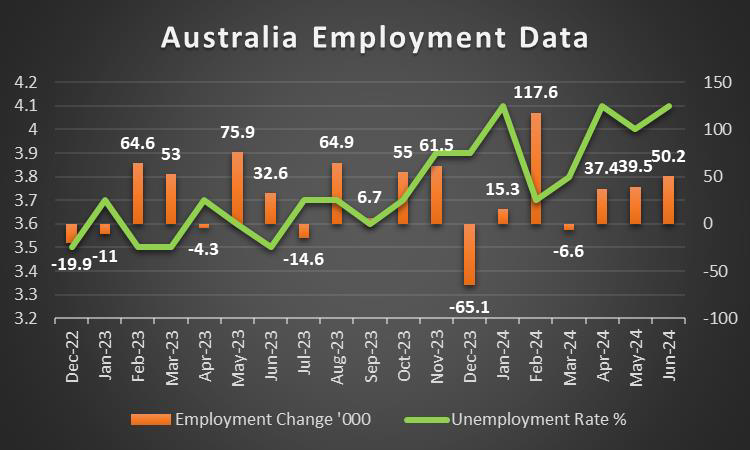

AUD – RBA opens the door for a rate hike

On a macreconomic level, we note that Australia’s service PMI came in lower than expected at 50.4, implying that Australia’s services sector of the economy expanded but at a slower pace than what was expected, which may imply that the services sector of the economy is slightly shaky. Nonetheless, the highlight of the week was the RBA’s interest decision in which the bank remained on hold, as was widely expected. As a reminder, AUD OIS in our last weekly report implied a 93% probability for the bank to remain on hold, yet the most interesting aspect of the bank’s decision was RBA Governor Bullocks press conference following the decision. In particular, RBA Governor Bullock stated that the bank is willing to raise interest rates should inflationary readings deviate from forecasted figures. Moreover, RBA Governor Bullock allegedly stated that a rate cut is not in the agenda in the near term, further enhancing the hawkish rhetoric that appears to have emerged from the bank. As such the bank’s hawkish rhetoric may aid the Aussie should it be maintained. For next week, we would also take a look at Australia’s employment data, where should it showcase a resilient labour market, it may aid the AUD and vice versa. We also note, as usual the deep economic ties between Australia and China on a fundamental level. Hence we that the release of China’s industrial output rate for July which is expected to increase to 5.5% from 5.3%, which may also aid the AUD, as it could imply an increase in raw materials stemming from Australia.

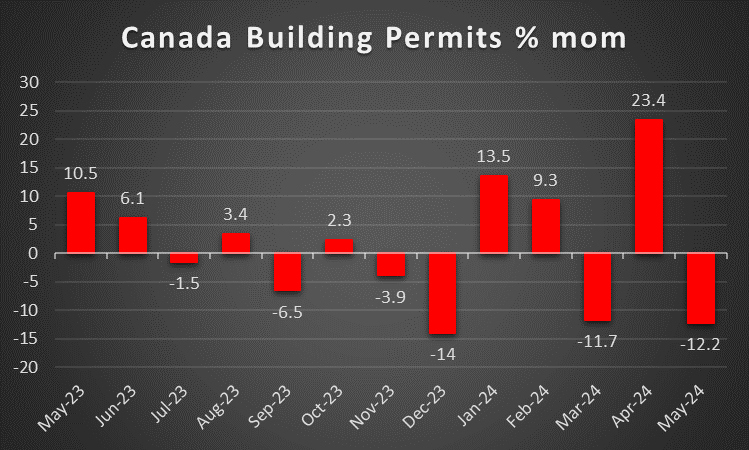

CAD – Building permits next week

In Canada, the Ivey PMI figure for July, came in lower than expected, which may imply that the manufacturing sector of the Canadian economy continues to expand, but at a slower pace than expected which could weigh on the Loonie should other financial releases imply a possible slowdown of manufacturing activity. As such, of Canada’s employment data which has yet to be released at the time of this report, may take an even greater importance, as should it showcase a loosening labour market, it may weigh on the Loonie and vice versa. On a fundamental level, we note that the recent geopolitical tensions stemming from the Middle East remain elevated which may aid oil prices and could provide some support for the CAD given Canada’s status as an oil exporting nation.

General Comment

As a closing comment, in the FX market we expect the USD to ceede some of its influence over other currencies as the frequence and gravity of US financial releases decreased. As for US stockmarkets, we note that that the unwinding of the carry trade and concerns about a recession in the US tended to weigh significantly on all three major indexes at the beginning of the week. We still maintain our concerns for the US stockmarkets and will continue to monitor them in the following week.As for gold prices we note that the lack of a significant military escalation between Israel and Iran may have led to some safe haven outflows, yet tensions still remain high and could quickly change over the weekend.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.