With the market having turned its engines to full mode with the new year, we are about to take a look at what next week has in store for the markets. On the monetary front, several policymakers from various central banks are to make statements and sway the market’s opinion. More specifically though, we highlight the release of BoJ’s interest rate decision on Wednesday, while we also note the release from Turkey of CBT’s interest rate decision on Thursday. As for financial releases we make a start on Monday with Japan’s corporate goods prices for December and Germany’s ZEW indicators for January. On Tuesday we get China’s GDP rate for Q4, UK’s employment data for November and Canada’s CPI rate for December. On Wednesday we get Japan’s machinery orders for November, UK’s CPI rates for December, the US retail sales for December and the Industrial production for the same month. On Thursday we get from Japan the trade data for December, Australia’s employment data for December and from the US the weekly initial jobless claims figure and the Philly Fed Business index for January. On Friday, we get Japan’s CPI rates for December, UK’s retail sales for December, Sweden’s GDP rate for December and Canada’s retail sales growth rate for November.

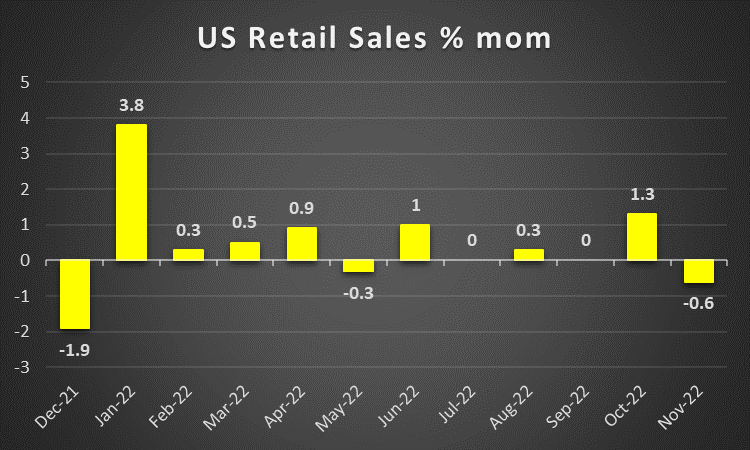

USD – Retail sales to catch the market’s attention

The USD is about to end the week, weaker than its counterparts. We have to note though that the release of the US employment report for December, last Friday, tended to support the idea that the US employment market is still tight given the drop of the unemployment rate and despite a drop of the NFP figure. The employment data tended to provide a green light for the Fed to maintain its hawkish stance. We should also note though that the release tended to provide a breath of life for the Fed’s expectations of a soft landing and St. Louis Fed President Bullard’s comments were characteristic on that. At the same time though the fact that the US CPI rates for December slowed down, tended to solidify the market’s expectations for an easing of the Fed’s aggressiveness and thus tended to weaken the USD. On the monetary front, we note that Powell’s speech at Sweden’s Riksbank symposium failed to actually excite traders as the Fed Chairman refrained from making any substantial statements about the outlook of the monetary policy of the bank. Nevertheless, the opinion that it’s time for the Fed to downshift to 25 basis points rate hikes seems to be gaining traction among Fed policymakers and Philadelphia Fed President Harker’s comments about this issue were characteristic. Philadelphia Fed President Harker stated that “Hikes of 25 basis points will be appropriate going forward” an opinion that was also shared by Atlanta Fed President Bostic. It seems that a consensus is slowly

building up within the Fed for the bank to start easing on its monetary policy tightening. Lastly, though we tend to note the worries created by the contraction of economic activity for the US services sector as marked by the release of the US ISM non-manufacturing PMI figure for December. Mind you that it’s the first contraction of economic activity for the US services sector since the pandemic. Similarly, also the drop of the factory orders growth rate into the negatives tends to intensify the worries for the manufacturing sector.

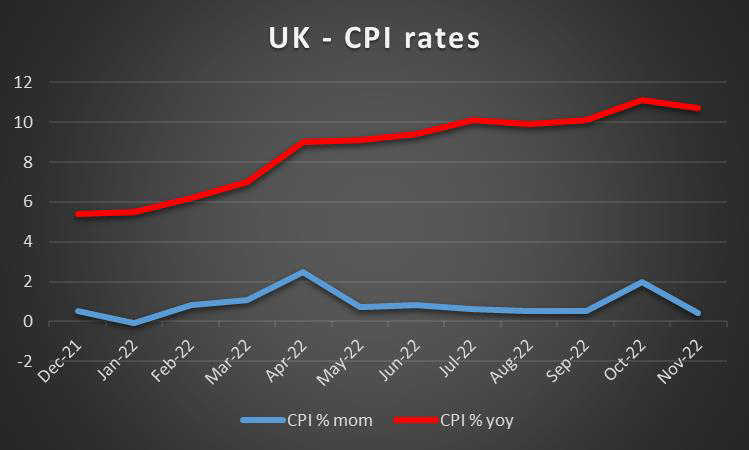

GBP – CPI rates and employment data

The pound is about to end the week stronger against the USD, seems to be edging lower against the JPY and is losing ground against the EUR. On a political level, Rishi Sunak managed to stabilize the situation in the last quarter of the year and ease the market’s worries about the UK Government’s intentions. On the other hand, the government still faces a huge cost of living crisis, and any efforts to boost the economy could intensify the inflationary pressures. At the same time, it should be noted that the international monetary fund is expecting the UK economy to grow at the slowest pace among other developed economies. Furthermore, we have to note that Brexit costs are ever present for the UK economy, while the war in Ukraine is ongoing implying that more military assistance will be required by the UK. On the monetary front, we note the worries of BoE’s Catherine Mann that the price caps on energy may be redirecting inflation in other areas. In a similar fashion BoE’s chief economist Hugh Pill, noted the risk of persistent inflation from the tight employment market despite the possible drop in energy prices. Hence, we tend to highlight the release of the CPI rates for December on Wednesday and the employment data on Tuesday.

JPY – BoJ’s interest rate decision in focus

JPY is about to end the week stronger against the USD, EUR and GBP, in a sign of a broader strength. The Japanese Yen got some support on Thursday after the release of a report stating that BoJ is to review in its next meeting the side effects of its ultra-loose monetary policy. The report also tends to maintain the view that more, efforts are to be taken to alter the Yield Curve Control (YCC) policy. It should be noted that the bank had altered YCC already in December as it rose the target yield of Japanese Government Bonds (JGB) to 0.50%, setting a higher threshold to actually intervene and start buying JGBs. In the coming week, we highlight the release of the Bank of Japan’s (BoJ) interest rate decision on Wednesday. The bank is expected to remain on hold keeping the interest at -0.10%, yet currently, JPY OIS provide only a 54.54% probability for such a scenario to materialize, that being only marginal, with the rest implying that a 10 basis points rate hike

is also possible. We expect that should the bank proceed with any tightening it may focus primarily on the YCC, rather than the interest rate as such. Also, some adjustment to the amount of bonds the bank is buying could be expected as the unlimited amount mentioned in the previous accompanying statement may be setting the bank in direct contrast with the markets. Overall we may see a subtle yet more concrete alteration of the bank’s ultra-loose monetary policy which could support JPY. Should the bank fail to proceed with any form of tightening, we may see JPY weakening.

EUR – Easy week ahead for EUR traders

The common currency is about to end the week stronger against the USD and the pound, yet seems to be losing ground against the JPY. The results of the week tend to showcase the influence that monetary policy differentials tend to have in the FX market. ECB seems to be sticking to its guns and is to maintain a hawkish approach regarding its monetary policy. It’s characteristic that ECB board member Schnabel stated that ‘Inflation won’t subside by itself,’ implying that more monetary policy tightening is required, while ECB’s chief strategist Philip Lane in a similar tone warned that inflation in the Eurozone, is to remain elevated, despite the possibility of rising energy costs starting to ease. Overall, we tend to maintain the view that ECB’s tightening is to continue on a steady basis and that could provide some support for the common currency, especially against the USD, as market expectations are for the Fed’s hawkishness to ease, currently. On a macroeconomic level, there are a number of signals that tilt on the positive side for the Eurozone, yet nothing conclusive yet. It’s characteristic that the industrial output of Germany got out of the negatives, for November, while Eurozone’s preliminary HICP rate for December slowed down below 10% reaching 9.2% yoy and the area’s retail sales growth rate for November accelerated getting out of the negatives. It seems as if the Eurozone is on the right track yet the worst may still be ahead, given ECB’s tightening.

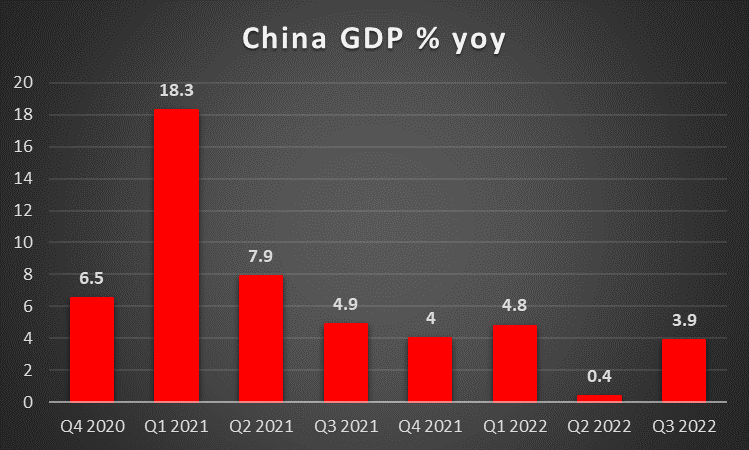

AUD – Australian employment and Chinese growth data in the epicenter

AUD is about to end the week stronger against the USD for the fourth time in a row. On a fundamental level, we note that China’s reopening may have provided some support for the Aussie, given also its second nature as a commodity currency and the fact that Australia exports a wide number of raw materials to China. China’s reopening is expected to be bumpy with the number of cases rising, yet in the grand scheme of things, is sending positive signals to the world markets as a possible economic recovery could soften the blow on a global level. In the coming week, we expect the markets to focus on the release of China’s GDP rate for Q4 2022 on Tuesday and a possible acceleration of the rate could improve the market sentiment, supporting riskier assets such as AUD. On a macroeconomic level, we note that the release of Australia’s CPI rates for November, held a surprise for Aussie traders as inflation accelerated on a year-on-year level for November while the retail sales growth rate accelerated beyond expectations showing that the average Australian consumer is willing and able to actually spend more in the Australian economy. The release could cause a more aggressive, hawkish stance on behalf of RBA, which had eased its hawkishness, especially given that the bank is to examine its interest rate decisions on a case-by-case basis. The next area of interest is the employment market with Australia’s employment data for December being due out on Thursday. Should the data show that the Australian employment market remains tight we may see the Aussie getting some support.

CAD – CPI rates and retail sales eyes

The Loonie is about to end the fourth consecutive week stronger against the USD. On a fundamental level, the rise of WTI prices could provide support for the CAD, given that Canada is a major oil producer. On the commodities front, we note that oil prices were on the rise yesterday, despite another massive rise of US oil inventories being reported for the past week, as hopes for increased demand from China surfaced. Analysts tend to mention that China’s needs for oil are rising substantially due to the new Lunar Year festivities and changes in its Covid policy. Should oil prices continue to be on the rise we may see the CAD getting additional support. On a macroeconomic level, we note the release of Canada’s employment data for December last Friday. The release highlighted the tightness of the Canadian employment market, as the unemployment rate ticked down instead of rising as expected and the employment change figure rose to a stellar 104.0k. The release tends to intensify market expectations for the bank to hike rates in its next meeting. It should also be noted that despite BoC’s rate hiking path, the building permits growth rate accelerated to 14.1% mom for November in a positive surprise for CAD traders, implying wider economic activity for the Canadian construction sector. In the coming week we highlight the release of Canada’s CPI rates for December on Tuesday and a possible acceleration could provide some support for the CAD as it could intensify the market’s expectations for a more hawkish BoC.

General Comment

In the coming week, we expect the USD to relent some of the initiative to other currencies, given that the frequency and gravity of US financial releases tend to ease. Such a development could allow for a more balanced blend of trading opportunities for market participants. Yet market attention may start shifting away from the FX market and towards the US equities markets, given that the earnings season has kicked off. Today we get the earnings releases of large banks namely JP Morgan, Bank of American and Citigroup, while the chorus of large banks is to continue on Tuesday with Goldman Sachs and Morgan Stanley. On Wednesday we note the release of the earnings report of Alcoa and on Thursday of Procter and Gamble as well as Netflix. A possible shift of the market’s attention may lower volatility in the FX market, while the lower number of high-impact financial releases may allow for fundamentals to take a more active role in the direction of the FX market. As for gold’s price please note that it’s about to end the week in the greens with the precious metal’s price benefiting from the weakening of the greenback. We expect the negative correlation of the two trading instruments to be maintained in the coming week and should the USD continue to weaken we may see gold’s price gaining further.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.