Yesterday’s session marked the end of the first month of 2023 with all three large cap US stock market indices closing in the greens, with Dow Jones 30 and S&P 500 paring most of their respective December losses, while the tech-focused Nasdaq 100 managed to end the month with more than 11% gains, rebounding from its December setbacks. Without a doubt the highlight for today is the Federal Reserve’s interest rate decision, followed by Fed Chair Powell’s speech. The market has already baked-in a 25-basis points rate hike and eagerly looks forward for the contents of the committee’s accompanying statement as well as the comments from the Chairman for guidance. In this report we aim to present the recent fundamental and economic news releases that impacted the US stock markets, look ahead at the upcoming events that could affect their performance and conclude with a technical analysis.

Fed’s interest rate decision in the spotlight

Today the FOMC is scheduled to convene, and the market awaits in anticipation for the first interest rate decision of this year from the Federal Reserve. The central bank has scaled down its interest rate magnitude to 50 basis points in December, after four straight 75 basis point increases and now the market foresees a 25-basis points hike. The view for a less hawkish approach stems from updated data indicating that inflationary pressures are abating, a robust employment market and better than expected growth results of the past quarter, alongside the explicit comments from some officials who favor a downshift. The increase by 25 basis points would bring the key policy rate to 4.75%, shy of 50 basis points from the terminal rate of 5.25%, indicated in the December’s dot plot graph. Market participants however, have increased their speculative bets throughout January forecasting that the central bank will not push rates as far as 5.25% and will be forced to cut rates around the start of the third quarter, as they anticipate that inflationary pressures will dissipate faster than expectations and the US economy will enter a “mild” recession. Since the market has almost fully priced in 25 basis points rate hike according to the FFF, the crucial aspect of the meeting is now the speech of Fed Chair Powell, alongside the forward guidance contained in the accompanying statement. Should there be a signal that the central bank is close to the end of its tightening cycle, the market may interpret that as dovish and we may see the dollar depreciate and in contrast, equities extend their climb to higher ground. Should however, we hear Fed Chair Powell push back on the narrative for looser financial conditions, adopting an unwavering hawkish stance, we may see the dollar strengthen and US stock markets move to the south.

Earnings roundup and upcoming releases

Even though, the Fed’s interest rate decision has the capacity to overshadow and outright dominate the direction of US stock markets, equity traders nonetheless continue to assess the earnings results of high-profile blue-chip companies. Yesterday, all three major US stock market indices, namely the Nasdaq 100, S&P 500 and Dow Jones 30 were on the rise, buoyed by speculations that the Fed will ease its monetary policy stance but also from upbeat earnings results by General Motors (#GM), Advanced Micro Devices (#AMD), UBS (#UBS), ExxonMobil (#XOM) and Pfizer (#PFE) among others. Earlier today, Snap (#SNAP) earnings

disappointed, and its share price was down by -14% in the pre-market session. Equity traders now shift their attention towards the earnings results of the tech giant Meta Platforms (#META) and China’s e-commerce behemoth Alibaba (#BABA). Furthermore, tomorrow’s earnings calendar is also packed with prestigious names such as Apple (#AAPL), Alphabet (#GOOG) and Amazon (#AMZN), alongside Ford (#F), Starbucks (#SBUX) and Shell (#SHEL), which are expected to keep traders on their toes.

Teknikal na Pagsusuri

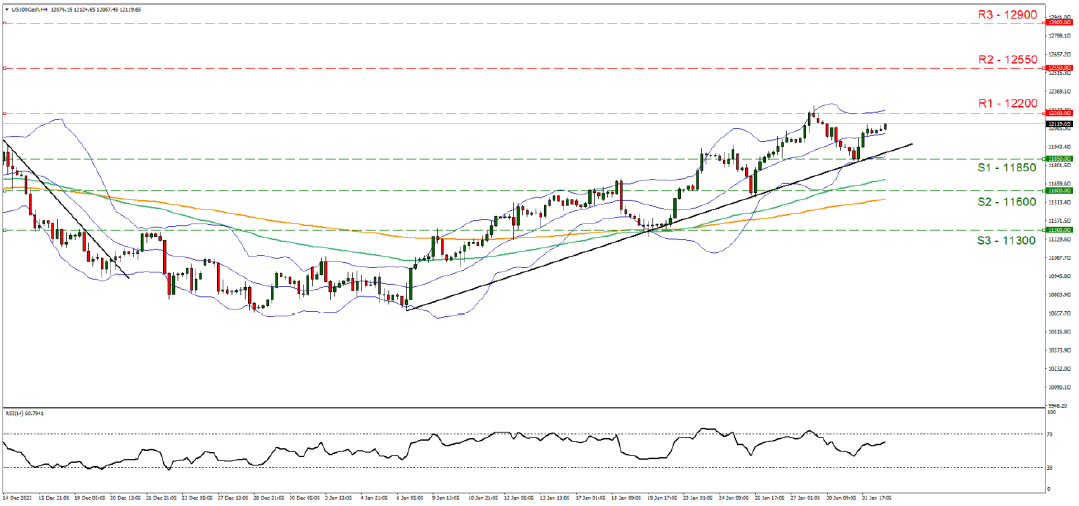

US100Cash 4-Hour Chart

Looking at #US100Cash 4-hour chart we observe the index extending its upward trajectory since the start of the year supported by speculations for a less hawkish Fed and a weaker dollar. We hold a bullish outlook bias for the index given the ascending trendline incepted since the 6th of January, yet we note that in the aftermath of the Fed’s interest rate decision later today could ignite a volatile reaction from the markets to either direction, depending on the announcement. Supporting our case is the RSI indicator below our 4-hour chart which showcases bullish sentiment in favour of the index. Should the bulls reign over, we may see the break above the 12200 (R1) resistance level and a move closer to 12550 (R2) resistance barrier. Should on the other hand the bears take over, we may see the break below the ascending trendline, the break of the 11850 (S1) support level and a move close to the 11600 (S2) support base.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.