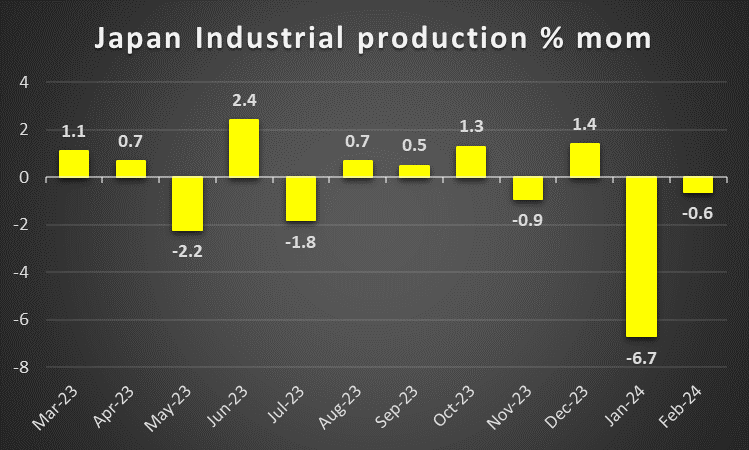

The week is about to draw to a close, hence we open a window at what next week has in store for the markets. On the monetary front, we highlight the release of the Fed’s interest rate decision on Wednesday, while we also note the interest rate decisions of Norgesbank from Norway and CNB from the Czech Republic, on Friday and Thursday respectively. As for financial releases, we note on Monday the release of Sweden’s GDP rate for Q1, Eurozone’s business climate for April and Germany’s preliminary HICP rate for April. On Tuesday we get Japan’s preliminary industrial output for March, China’s NBS and Caixi manufacturing PMI figure for April, Australia’s retail sales for March, France’s preliminary GDP and HICP rates for Q1 and April respectively, Switzerland’s KOF indicator for April, the preliminary GDP Rate for Q1 of the Czech Republic, Germany and the Eurozone as well as the preliminary HICP rate of the Eurozone for April and Canada’s GDP rate for February. On Wednesday we get New Zealand’s employment data for Q1 and from the US we note the release of the ISM manufacturing PMI figure for April. On Thursday we get Australia’s building approvals for March, UK’s Nationwide House Prices for April, Switzerland’s CPI rates for April, Canada’s trade data for March, and from the US the weekly initial jobless claims figure and March’s factory orders. On Friday we note the release of Turkey’s CPI rates for April, from the US the ISM non-manufacturing PMI figure for April and we highlight the release of the US employment report for April.

USD – Fed’s interest rate decision and April’s employment data

The USD seems about to end the week in the reds against its counterparts, yet March’s Core PCE rates are still to be released and could affect its course. In the coming week, we may see the USD being moved by the release of the Fed’s interest rate decision. The bank is widely expected to remain on hold and currently Fed Fund Futures (FFF) tend to imply a probability of 97.4% for such a scenario to materialise. Hence we expect the market’s attention to turn towards the accompanying statement and Fed Chairman Powell’s press conference for any clues regarding the bank’s future intentions. It should be noted that FFF also imply that the market expects the bank to start cutting rates in the September meeting. Yet inflation seems to be sticky and may be adding pressure on the bank to maintain rates high for longer. Should the bank’s forward guidance imply a possible delay of any rate cuts we may see the market’s expectations being contradicted and the USD getting some support. On the flip side should the bank indirectly verify the market’s expectations, we may see the USD losing ground. The second market-moving event is expected to be the release of the US employment report for April. Should the report show that the US employment market remains resilient, we may see the USD getting some support and vice versa. Please note that both the Fed’s interest rate decision as well as the release of the US employment data for April, could have ripple effects beyond the FX market also on US stockmarkets and the price of gold. Finally, we would like to note the release of the ISM manufacturing and non-manufacturing PMI figures for April on Wednesday and Friday respectively. Despite the possibility of the ISM PMI figures being overshadowed by the Fed’s interest rate decision and the release of the US employment report for April, we still note the releases as macroeconomically important and should the indicators show a faster expansion of economic activity in the respective sectors of the US economy we may see the USD getting some support and vice versa.

GBP – Fundamentals continue to lead the pound

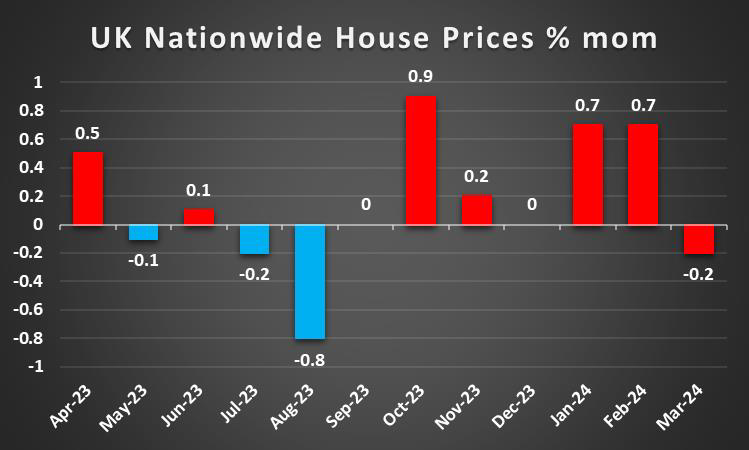

The pound is about to end the week higher against the greenback and the Yen, yet loses ground against the common currency. In the coming week, we note a rather easy calendar for pound traders regarding financial releases, maybe with the most notable being the nationwide house prices for April. A possible acceleration of the relative growth rate could imply a wider demand for housing in the UK which could be considered a positive for the pound. Also notable would be the final figures of April’s PMI indicators on Friday. Given the lack of high-impact financial releases in the coming week, we expect the pound to be mostly fundamentally driven. On a monetary level, we note the market’s current expectations for the bank to cut rates twice this year, starting from the August meeting. Yet the bank seems to be taking its time before proceeding with any rate cuts. Despite the bank expressing its optimism that inflation is to slow down further in the current month, the actual CPI rate is still substantially higher than the bank’s inflation target of 2%. It’s characteristic that BoE’s chief economist Hugh Pill stated practically that any rate cuts are still a way off, as he also expressed his worries for the possibility of the bank cutting rates too early as greater risks could emerge regarding inflation in the UK economy. The comment tended to lean on the hawkish side and may have pushed back against market expectations for the bank to cut rates. The bank’s next meeting is scheduled for the 9th of May and until then we may see market expectations about the bank’s intentions being influenced by analysts.

JPY – BoJ signals continuance of easy policy

JPY is about to end the week weaker against the GBP, the EUR and the USD, in a sign of wider weakness. On a macroeconomic level, we note that economic activity in Japan seems to have improved in the current month according to the preliminary PMI figures. On the demand side, the acceleration of the Chain store sales for March highlighted its resilience, which may also imply a continuous feeding of inflationary pressures in the Japanese economy. Yet Tokyo’s CPI rates slowed down beyond market expectations, foreshadowing further easing of inflationary pressures in the Japanese economy as a whole. On a monetary level, BoJ released its interest rate decision during today’s Asian session and as was widely expected remained on hold, keeping rates at 0-0.1%. Also, the bank highlighted its conviction that inflation rates are to remain near the bank’s targets, in a rather optimistic note. The bank also tended to signal that it’s prepared to hike rates further near the end of the year. Yet at the same press conference BoJ Governor Ueda also stated that the bank is to maintain easy financial conditions for the time being. Overall, the lack of clear forward guidance, given that the accompanying statement was exceptionally short, even for BoJ’s standards, tended to weaken the JPY further. Yet on a fundamental level, the possibility of a market intervention to JPY’s rescue, is now clearly on the horizon. The possibility of the Japanese Government actually intervening in the markets seems to have increased after Japan, S. Korea and the US have agreed to “consult closely” on foreign exchange markets, which could be perceived as a green light by the US for a market intervention. Yet we repeat our skeptisism, not on the possibility of a market intervention per se, but on its usefulness as the positive effect for JPY may prove to be temporary, as BoJ’s dovishness remains intact and may reignite the weakening of JPY.

EUR – GDP and HICP rates to move EUR

The common currency is about to end the week, stronger against the USD, the GBP and JPY, in a sign of wider strength. On a macroeconomic level, we note that the improved economic activity on a Eurozone level, may have been unterpinned by the services sector rather than the manufacturing sector, as per the preliminary PMI figures for April. The mixed signals intensified as Germany’s business climate seems to be improving yet in France seems to be deteriorating. In the coming week, we highlight the release of the preliminary HICP rates for April. Should the rates slow down further nearing the ECB’s target of 2%, we may see the EUR slipping as it would ease resistance for the bank to proceed with its first rate cut in its June meeting. Furthermore, we also note the release of the preliminary GDP rates for Q1 and a possible slowdown, even contraction of the rates could weigh on the EUR as the specter of a recession may worry EUR traders. On the monetary front, we note the market’s expectations for the bank to proceed with its first post-pandemic rate cut in the June meeting and deliver another one, maybe two, until the end of the year. Yet there seem to be worries among ECB policymakers that the last mile may prove to be more bumpy than expected. In particular, the ECB seems to be concerned about prices in the services sector and should the HICP rates fail to slow down as expected, we may see the bank’s stance hardening, possibly even putting a potential rate cut on ice in its next meeting on the 8th of May.

AUD – Market sentiment to move the Aussie

AUD recovered the losses of last week and is about to end the week in the greens against the greenback. On a macroeconomic level, we note the improvement of economic activity in Australia, according to the preliminary PMI figures for April. Yet the highlight of the past few days for Aussie traders, may have been the substantial easing of inflationary pressures in the 1st quarter of the year. The easing of inflationary pressures may allow RBA to ease on its hawkishness. Yet the market does not seem to expect any rate cuts to be delivered by the bank until the end of the year. Nevertheless, we note that the CPI rate has neared the bank’s target range for inflation of 1.00%-3.00%. On a fundamental level, we note the market’s perception of the Aussie being of a riskier nature as a commodity currency. Hence should the market sentiment tend to improve, we may see the Aussie getting some support while a more risk-averse approach of the market may weigh on the Aussie. In the coming week, we do not have any heavy-impact financial releases scheduled for Aussie traders, hence we expect fundamentals to lead the Aussie. Remaining on the fundamental level of the Aussie we also highlight the close Sino-Australian economic ties. In the coming week, we note the release of China’s NBS and Caixin manufacturing PMI figures for April. Should both indicators remain above the reading of 50, they would align in implying an expansion of economic activity for the huge Chinese manufacturing sector. Such an expansion may provide support for the Aussie as it may imply more exports of raw materials from Australia to China.

CAD – February’s GDP rate eyed

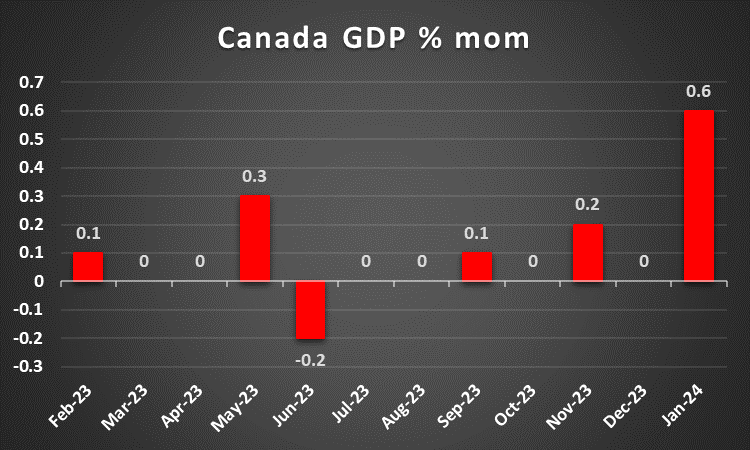

The CAD is about to end the week slightly stronger for a second week in a row. On a fundamental level, we note that a possible improvement of the market sentiment may provide some support for the CAD as well. Also, we note that oil prices seem to have halted their drop which may have also provided some support for the Loonie. We note that the supply side of the international oil market tends to be rather tight and should oil prices rise in the coming week, they may provide some support for the Loonie given Canada’s as a major oil-producing economy. On a macroeconomic level, we note that despite an improvement of the retail sales growth rate for February, the rate remained in the negatives, which may have been disappointing on a macroeconomic level. On the inflation front, we note that prices rose faster than expected on a month-on-month level for producers for March. In the coming week, we note the release of the GDP rate for February and a possible acceleration could brighten the economic outlook of Canada and provide some support for the Loonie. Also, the release of the manufacturing PMI figure for April and Canada’s trade data for March could catch Loonie trader’s attention. On a monetary level, we note the release of BoC’s deliberations for the April meeting. The document on the one hand, tended to lean on the dovish side as the bank seems to recognise the easing of inflationary pressures in the Canadian economy. Characteristically the document stated that policymakers “were encouraged by the recent progress on CPI and core inflation”. On the other hand, there are still worries for the potentially inflationary pressures caused by oil prices causing a number of policymakers to hesitate to start cutting rates.

General Comment

Overall we tend to expect the USD to increase its influence over other currencies in the FX market, as the gravity and frequency of US stemming financial releases increases. Volatility though in general for the FX market is expected to rise as we get high-impact financial releases from other countries as well, which may allow some currencies to escape USD’s influence and come under the spotlight. As for US equities, we note that on a fundamental basis, market worries that inflationary pressures in the US economy may prove to be persistent and force the Fed to maintain rates high for longer seem to be weighing. Yet it should be noted that major US stock market indexes sent out mixed signals. We expect though that besides the fundamentals surrounding US stock markets and the US financial releases, the earnings reports of high-profile companies may also catch the market’s attention. In the coming week, we note the release of the earnings reports of NIO (#NIO), 3M (#MMM), Starbucks (#SBUX), Coca Cola (#KO), McDonalds (#MCD), Pfizer (#PFZ), eBay (#EBAY), Airbnb (#ABNB), Shell (#Shell) and Apple (#AAPL). On the other hand, gold’s price is about to end the week in the reds. It should be noted that the negative correlation of the USD with gold’s price was not present in the current week, and we may see that relationship being interrupted in the coming week as well.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.