Definitely the highlight of the coming week is to be the US elections on Tuesday. The stakes are extremely high and with the race of the office of the Presidency, House of Representatives, Senate and Governorships at stake, other financial releases may be overshadowed by the political spectacle that is set to occur in the US.

USD – US Election on Tuesday

On a political level, one of the most widely anticipated events of the year is set to occur next Tuesday. In particular, we have the US Presidential elections which are set to take place on the 5th of November, alongside elections for the House of Representatives, Senate and for state Governor. Overall in the event of a Trump win, we may see the dollar strengthening given the potential positive implications for the dollar, based on the former president’s policies. However, should we see a delay in the results or votes being contested, the political turmoil that would ensure, could weigh on the dollar.

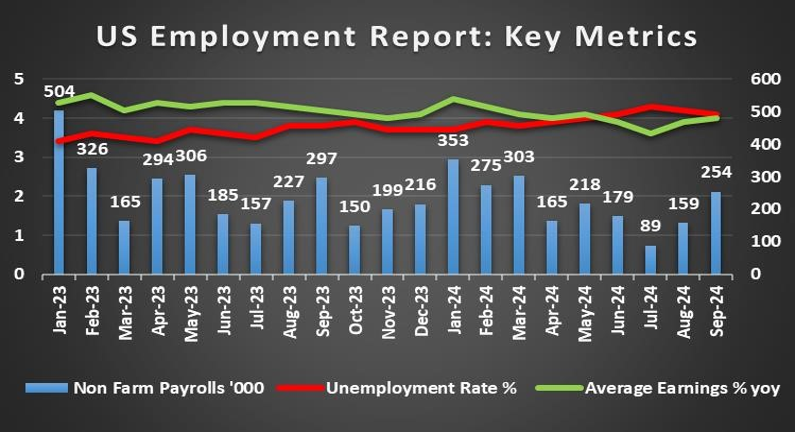

On a macroeconomic level, the US employment data has yet to be released and could easily influence the dollar’s direction. Generally speaking, should the employment data showcase a resilient labour market it may support the dollar and vice versa. In other financial releases, the Core PCE rates for September which are the Fed’s favourite tool for measuring inflationary pressures came in hotter than expected, which may increase calls for the Fed to withhold from aggressively cutting interest rates in the near-term. Thus, the implications of persistent inflationary pressures in the US economy may have aided the greenback.

Analyst’s Opinion (USD)

“The Fed’s decision is usually the highlight of the week, yet this time we look towards the US Presidential Elections. No clear winner has emerged and with a variety of scenarios being floated such as a red or blue sweep we remain extremely vigilant as we eagerly await to see who will win the Presidential Elections. In our view, we would not be surprised to see delays as certain swing states may be decided by a very narrow margin which in turn may lead to calls for a recount. Generally speaking, if political instability ensues following the election such as calls of election fraud or a refusal to certify the results or even a delay, we may see the greenback weakening

GBP – BoE decision next week

On a fundamental level, the new Labour Government has finally unveiled their long-awaited Autumn budget. According to some media outlets, the UK’s finance minister has delivered the biggest tax hike package in three decades at an incredible figure of £40 billion, with businesses and wealthy individuals appearing to be most heavily affected by the new tax increases. Overall, the jury is still out on the budget and thus we may see increased volatility in the pound next week.

On a monetary level, the BoE’s interest rate decision is set to occur next Thursday, with the majority of market participants currently anticipating the bank to cut interest rates by 25 basis points. Specifically, GBP OIS currently implies an 81.5% probability for such a scenario to materialize. As such our attention turns to the bank’s accompanying statement, where should it be implied that the bank will continue on their rate cutting cycle, it may weigh on the pound and vice versa.

Analyst’s Opinion (GBP)

“The BoE’s decision is due out next Thursday with policymakers possibly scrutinizing the Government’s report in order to gauge its impact on the economy. In our view, the increase in Government spending may increase pressure on the bank to withhold from cutting interest rates once again, or issue a warning that they may have to withhold from aggressively cutting interest rates”

JPY – BOJ remains on hold

Monetary-policy-wise, we would like to note that the BOJ’s interest rate decision occurred this week, with the bank keeping interest rates steady at 0.25% as was widely expected by market participants. Market interest may have shifted to BOJ Governor Ueda’s comments following the bank’s decision in which he stated that “As for the timing of the next rate hike, we have not preset idea”, implying that the bank has no preset rate path, which in turn may have weighed on the JPY.

On a political level, we must note the Japanese elections on Sunday, where voters delivered a blow to Japan’s liberal democratic party which has governed almost continuously since 1995. Following the elections the LDP has lost its parliamentary majority in the lower house for the first time in 15 years. Hence, in order to remain in power, the LDP may need to broaden its coalition and even in such a scenario, Prime Minister Ishiba’s position is still in jeopardy. Overall, the political instability may weigh on the JPY .

On a macroeconomic level we note Japan’s Tokyo CPI rates which came in hotter than expected at 1.8% yet when compared to last month’s rate of 2.0%, it could be inferred that inflationary pressures in the Japanese economy may be easing, which in turn may have eased pressure on the BOJ to hike interest rates in their last meeting.

Analyst’s Opinion (JPY)

“The BOJ’s decision to remain on hold, was strategic in our view, as despite a hotter-than-expected inflation print last Friday, it did not necessitate a response by the bank. Furthermore, the BOJ may be looking for the dust to settle in the political landscape in order to better adjust their monetary policy path as the nation enters uncharted waters from a political perspective.”

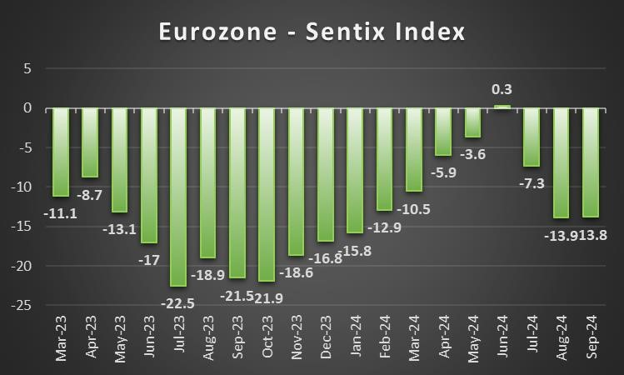

EUR – Upbeat Eurozone

On a monetary policy level ECB policymakers appear to be facing a dilemma. In particular ECB member Panetta implied earlier on this week that monetary conditions remain restrictive and that rates need to come down. Yet, when looking at this week’s financial releases, the case for the ECB to continue on its aggressive rate-cutting path may have decreased.

In particular, the preliminary GDP rates for Germany, France, and the Zone came in higher than expected, which may have aided the EUR, as signs of economic resilience appear to have emerged. Furthermore, of interest was Germany’s preliminary GDP rate for Q3 on a QoQ basis which by coming in higher than expected, allowed Germany to narrowly avoid a technical recession. Furthermore, the preliminary HICP rates for France, Germany and the Zone, also came in hotter than expected implying persistent inflationary pressures and thus may have mitigated calls for the ECB to continue cutting rates aggressively, which in turn may aid the EUR.

Analyst’s Opinion (EUR)

“If the Eurozone stays on its current path, the case for the ECB to aggressively cut interest rates may diminish. Moreover, of concern was the overall acceleration of inflation in the Zone, as should it fail to come down to the bank’s 2% inflation target it may spell trouble for the ECB.”

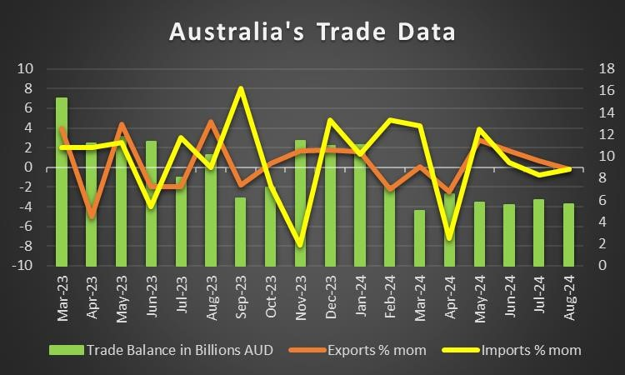

AUD – RBA decision next week

On a macroeconomic level, Australia’s CPI rate on a yoy level came in hotter than expected at 2.8% versus the expected 2.3%, yet remained lower than last month’s rate of 3.8%. The implications of easing inflationary pressures in the Australian economy could have increased pressure on the RBA to cut interest rates in their meeting next week. Yet, the failure to ease to 2.3% may be a source of concern for policymakers and thus may intensify calls for the bank to remain on hold

In particular, the majority of market participants are currently anticipating the bank to remain on hold at 4.35% with AUD OIS currently implying a 96.3% probability for such a scenario to materialize. As such attention may turn to the bank’s accompanying statement where should it imply that the bank may cut interest rates in its next meeting, it could weigh on the AUD and vice versa.

Analyst’s Opinion (AUD)

“The CPI rates are in a goldilocks zone where they imply easing inflationary pressures, yet not to the degree that may warrant a rate cut by the RBA in their meeting next week. In our view, we tend to agree with the majority of market participants that the RBA may remain on hold, yet with inflation now below 3% and closer to the bank’s 2% target, we would not be surprised to see a dovish undertone in the bank’s accompanying statement”

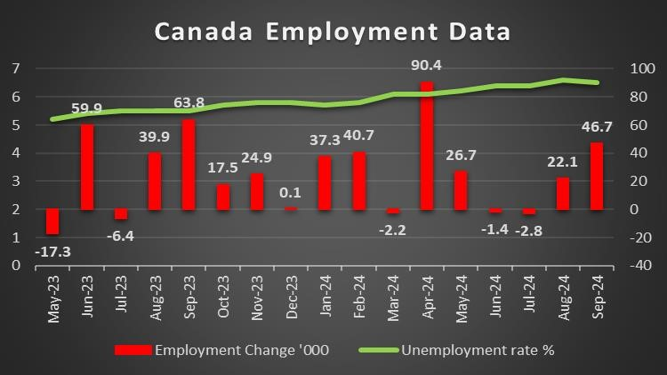

CAD – Employment data next week

The main factor affecting the Loonie in the past few days may have been the release of Canada’s retail sales rate which came in much lower than expected at -0.7% and thus may spark concerns over the resiliency of the Canadian consumer. For next week, we would like to point out Canada’s employment data where should a resilient labour market be showcased, it could aid the Loonie and vice versa.

On a fundamental level, we note that Prime Minister Trudeau was given a deadline to step down by the 28th of October, following a letter which was signed by 20 lawmakers who called on the Prime Minister to step down. It now appears according to Reuters that Trudeau has managed to secure his immediate political future, when a leader of a smaller political party did not join efforts to bring down the minority Liberal Government.

Analyst’s Opinion (CAD)

“The political turmoil within Canada may be an issue for Loonie traders should it resurface, yet for now it appears that the CAD has been spared from the effects of an early election. Moreover, we are still concerned about Canada’s economy, and look towards next week’s employment report to garner more information in regards to the healthiness of the Canadian labour market ”

General Comment

As a closing comment we remain concerned about the high number of fundamental issues tantalizing the markets. The central bank decision from the US, could in itself increase volatility in the markets. However, the biggest event may be the US Presidential Elections which are set to occur next week. Thus with the stakes this high, and no clear winner having emerged, we would not be surprised to see a significant increase in volatility next week. As for gold we note that the precious metal formed new-all time highs once again earlier on this week, and that its correlation with the dollar appears to be mending, with the dollar moving lower for the week whilst the precious metal moved higher. On a geopolitical level, there have been recent allegations that Iran may be preparing to retaliate against Israel. In our view, Israel’s response and decision not to strike Iranian nuclear and oil facilities was calculated in an attempt to prevent a further escalation in the region and thus the recent claims that Iran may retaliate could simply be Iran trying to save face.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.