In the coming week the calendar seems to be getting heavier. On the monetary front we note the BOJ’s interest rate decision on Thursday. In terms of financial releases, we make a start on Tuesday with Sweden’s preliminary GDP rate for Q3 and the US JOLTS Job openings figure for September. On Wednesday we note Australia’s CPI rates and France’s preliminary GDP rate both for Q3, Switzerland’s KOF indicator for October, the Czech Republic’s, Germany’s and the Eurozone’s preliminary GDP rates for Q3, the US ADP national employment figure for October, the US preliminary GDP rate for Q3 and Germany’s preliminary HICP rate for October. On Thursday, we note Japan’s preliminary industrial output rate for September, Australia’s retail sales rate, China’s NBS manufacturing PMI figure, France’s and the Eurozone’s preliminary CPI and HICP rates respectively all for October, followed by the US Core PCE rates for September, the US weekly initial jobless claims figure, Canada’s GDP rate for August and New Zealand’s unemployment rate for Q3. Lastly on Friday, we get China’s Caixin manufacturing PMI figure, Switzerland’s CPI rate, the UK’s manufacturing PMI figure, the US Employment data, Canada’s manufacturing PMI figure and the US ISM Manufacturing PMI figure all for the month of October.

USD – It’s going to be a very busy week for the USD

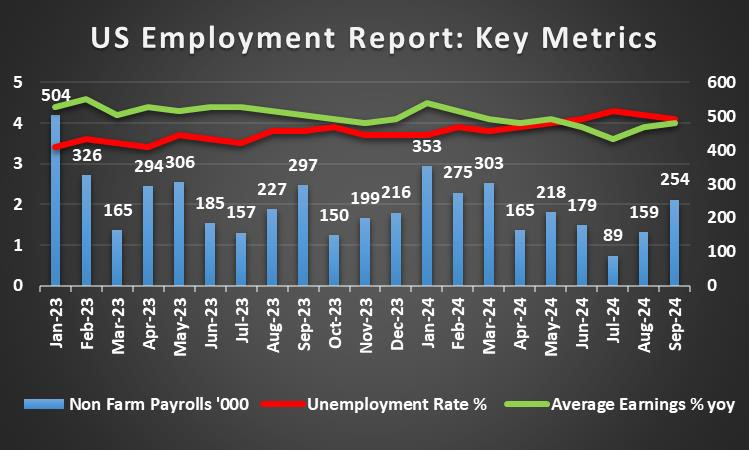

• The main factor behind USD’s movement in the past week may have been the Fed’s monetary policy once again. Fed policymakers continued to cast doubt on the market’s expectations for two more rate cuts by the bank by the end of the year, which may have aided the greenback.

• On a macro-economic level, next week is going to be a roller coaster ride for dollar traders. In particular, we have the US employment data for October, the preliminary GDP rate for Q3 and the Core PCE rates for September which is the Fed’s favourite tool for measuring inflationary pressures. Overall, should the financial releases showcase a resilient US economy and labor market, or persistent inflationary pressures, it may provide the Fed with some leeway to withhold from aggressively cutting interest rates. In turn this may aid the dollar, as the two-rate cut expectations by market participants may be reduced. Whereas should cracks appear in the US economy’s armour, it may increase pressure on the Fed to cut interest rates further which may weigh on the dollar.

• On a fundamental level, we are less than 14 days away from the US Presidential Elections. The race is still too close to call and thus we may see increased volatility in the markets if one candidate manages to take a clear lead in key -swing states.

Analyst’s Opinion (USD)

“We remain vigilant to other factors that may influence the dollar other than the Fed, as election season is heating up. Moreover, financial releases stemming from the US next week, could lead to a roller-coaster ride for the greenback and thus we would approach next week by focusing on one day at a time”

GBP – UK PMI figures disappoint

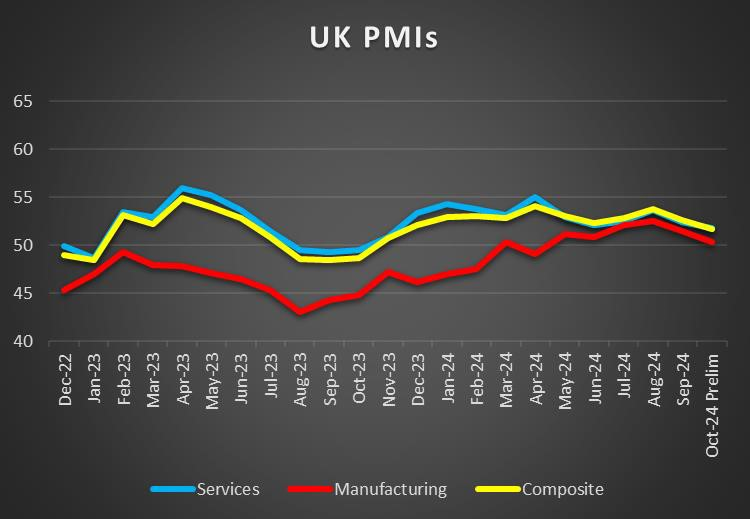

• Economic data shook the pound in the past few days. The UK’s preliminary Composite, Services and Manufacturing PMI figures for October came in lower than expected. The lower-than-expected PMI figures may imply that the UK economy is not as resilient and thus may have weakened the pound this week. In terms of financial releases next week, we note no major financial releases from the UK, hence we may see fundamentals leading the way for the sterling.

• On a monetary level, BoE Governor Bailey according to the FT, stated earlier on this week that he was seeing a “good story” in regards to slowing down headline inflation rates. In turn, the apparent comment that progress has been made in combating inflationary pressures in the UK economy, may increase pressure on the BoE to continue on its rate cutting cycle and potentially act even more aggressively which could weigh on the pound.

Analyst’s Opinion (GBP)

“Despite the preliminary PMI figures remaining above contraction territory, we remain concerned about the resiliency of the UK economy. Moreover, with inflation at 1.7% yy which is below the bank’s 2% inflation target, we would not be surprised to see further BoE policymakers in the coming week, adopt a more dovish tone, which could weigh on the pound”

JPY – More rate hikes to come?

• Monetary-policy-wise, we highlight the comments by BOJ Governor Ueda earlier on this week, who hinted that more rate hikes are to come. Essentially, BOJ Governor Ueda appears to be concerned as to which path would be best for the bank to continue hiking interest rates, and in his own words stated that “if you proceed very, very gradually and create the expectation that rates are going to stay at low levels for a very long period, this could lead to a buildup of huge speculative positions — which could become a problem later.

”In conclusion, BOJ Governor Ueda’s comments may be perceived as hawkish in nature which in turn may aid the JPY.

• Moreover, the BOJ’s interest rate decision is set to occur next week, with the majority of market participants currently anticipating the bank to remain on hold at 0.25% with JPY OIS currently implying an 83.8% probability for such a scenario to materialize. In turn, this may weigh on the JPY.

• On a macroeconomic level we note Japan’s Tokyo CPI rates which were released earlier on today, yet we would emphasize that the BOJ’s decision we mentioned above may take centre stage for Yen traders next week.

• Political uncertainty seems to be high given the elections in Japan over the weekend. The importance of the elections may also rely in the assumption that the outcome could affect also BoJ’s efforts to normalise its monetary policy. It should be noted that the ruling Liberal Democratic Party’s (LDP) long-standing dominance may be shaken, yet seems set to survive the elections. Nevertheless should the LDP lose points in the elections some uncertainty may arise and the party may harden its stance, exercising pressure on BoJ to abandon its rate hiking plans. Hence the conjunction of fundamental uncertainty both on a political and monetary level, tends to cause JPY to wobble.

Analyst’s Opinion (JPY)

“The BOJ’s interest rate decision next week may take the markets by surprise. Despite JPY OIS currently implying an 83.8% probability for the bank to remain on hold, we remain concerned about the comments made by BOJ Governor Ueda and in particular the concerns about creating the expectations that rates are going to stay at low levels for a very long period. Hence, we would not be surprised if the BOJ opts for a surprise rate hike in their meeting next week ”

EUR – HICP and GDP rates in focus

• On a monetary policy level ECB President Lagarde earlier on this week stated that “the direction of travel is clear” when referring to the ECB’s monetary policy path, which may imply that the bank will continue on its rate-cutting cycle. Moreover, ECB Chief Economist Lane’s comments appear to have echoed ECB President Lagarde’s overall implied rhetoric, that the current economic conditions may be favourable for the bank to maintain its monetary policy approach of cutting interest rates. In turn, the relatively overall dovish sentiment may have weighed on the common currency.

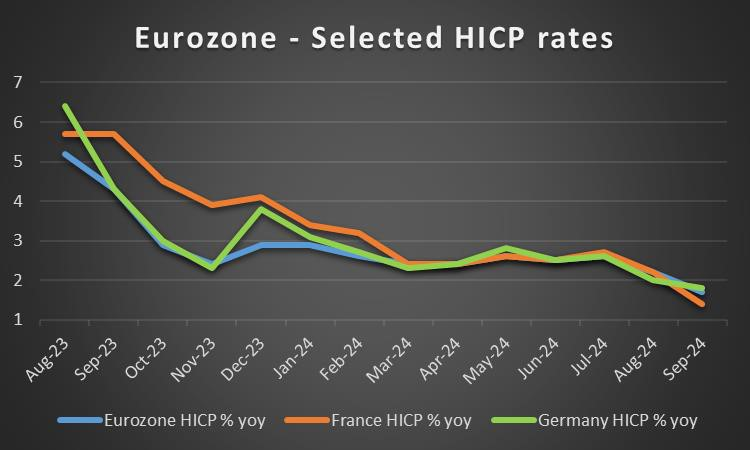

• As for financial releases we highlight the preliminary PMI figures for August which were released yesterday. In particular France’s services PMI figure came in lower than expected, implying that France’s

services sector of the economy is diving deeper into contraction territory. Yet, Germany’s manufacturing sector came in better than expected , implying a narrower than expected contraction in the country’s manufacturing sector. Overall, the mixed financial releases may have temporarily aided the EUR, yet traders may be more interested in next week’s financial releases and in particular the zone’s preliminary GDP rate for Q3 and the preliminary HICP rates for October.

Analyst’s Opinion (EUR)

“The EUR will be put to the test next week, with the GDP and HICP rates taking the stage for EUR traders. In particular, we would like to focus on, the inflation print, which should it fail to slowdown or remains relatively unchanged, it may increase pressure on the ECB to ease off their rate cutting cycle. We tend to view the HICP rate as crucial, as should inflationary pressures in the zone fail to tick down, it could cast doubt and we may see concerns emerging that the ECB may have been premature in cutting interest rates”

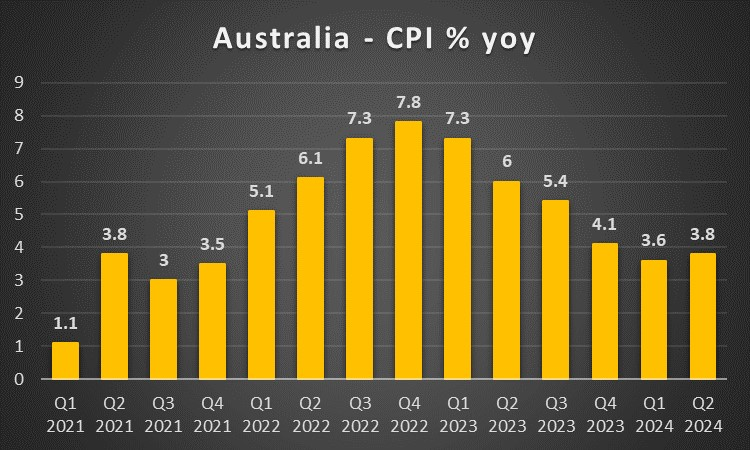

AUD – CPI rates in sight for Aussie traders

• On a macroeconomic level, Australia’s preliminary manufacturing figure for October was released yesterday. Specifically, the figure came in at 46.6 which is lower than last month’s figure of 46.7 and tends to imply a further contraction of the manufacturing sector and thus may have aided to the Aussie’s weakening this week.

Nonetheless, interest may pick up next week with the release of Australia’s CPI rate for Q3. Should the CPI rates showcase easing inflationary pressures in the Australian economy, it may increase pressure on the RBA to pivot towards a more dovish stance in their next meeting which may weigh on the AUD. Whereas a hotter-than-expected inflation print, could sway the RBA to consider a rate hike, which instead could aid the AUD.

• On a monetary level we note the comments made by RBA Deputy Governor Hauser earlier on this week who appears to have echoed the hawkish remarks from RBA Assistant Governor Hunter last week that inflation is still “too high” in the Australian economy. In turn should further RBA policymakers echo the hawkish rhetoric that appears to be emerging from the RBA, it could aid the AUD.

Analyst’s Opinion (AUD)

“The RBA has kept the door open for either a rate cut or a rate hike during their last monetary policy meeting. As such, with recent RBA policymakers stating that inflation remains too high, the release of the CPI rates next week may be a pivot moment for RBA policymakers in terms of their next monetary policy decision in November. Yet given other financial releases and in particular those from the US, it could overshadow the release of Australia’s CPI rates”

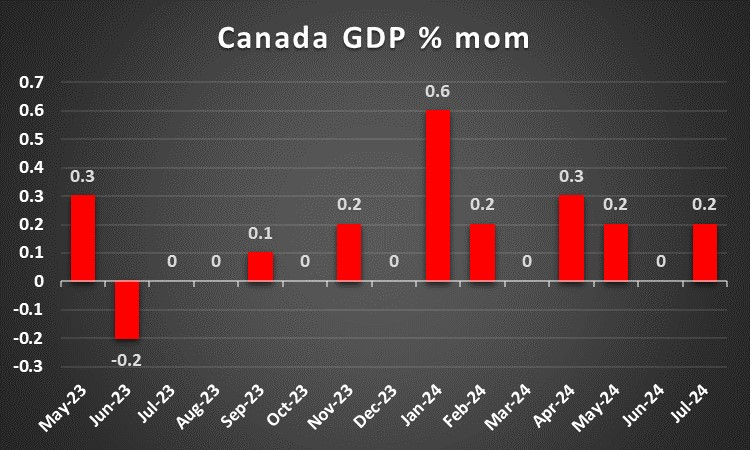

CAD – BoC cuts by 50bp as expected

• The main factor affecting the Loonie in the past few days may have been the release of the BoC’s interest rate decision in which the bank cut interest rates by 50 basis points, as it was widely expected. In the bank’s accompanying statement, it was stated that “If the economy evolves broadly in line with our latest forecast, we expect to reduce the policy rate further”. Essentially implying that the bank may continue on its monetary easing cycle, which in turn may weigh on the Loonie.

• On a macroeconomic perspective, we would like to note for Loonie traders the release of Canada’s manufacturing PMI figure for October next Friday. Should the PMI figure come in higher than last month’s figure of 50.4,it may aid the Loonie and vice versa.

• On a fundamental level, we note that Prime Minister Trudeau has been given a deadline to step down by the 28th of October, following a letter signed by 20 lawmakers who called on the Prime Minister to step down. However there are 153 liberal members of the parliament which may imply that the calls for the PM to step-down may lack widespread support. Nonetheless, should the Prime Minister step down, the political uncertainty that could ensue may weigh on the CAD.

Analyst’s Opinion (CAD)

“The BoC cut interest rates as was expected, and with the comments made by the bank we would not be surprised to see the BoC continuing on its monetary easing cycle. Our interest currently is the possibility of a political mutiny against PM Trudeau who is 19 points behind his Conservative rival in a CBC poll tracker. We would not be surprised to see division within the PM’s party, which in turn could lead to political instability in Canada which in turn could weigh on the country’s currency. ”

General Comment

As a closing comment we remain concerned about the high number of fundamental issues tantalizing the markets. The high number and important financial releases from the US, EU and Japan could heavily increase volatility in the markets. Hence we tend to maintain the view that the markets may remain extremely sensitive and possibly overreact from one financial release to the other. In the coming week, we expect the USD to regain some of the initiative in the FX market, given that the gravity and frequency of US financial data increases. As for US stock markets, the earnings season is in full swing creating headlines and catching market participants attention. In the coming week we note the earnings releases of Visa (#V), Pfizer (#PFE), McDonalds (#MCD) and Google (#GOOG) on Tuesday. On Wednesday we get Airbus (#Airbus), Meta (#FB), Microsoft (#MSFT) and eBay (#ebay). On Thursday we get Intel (#INTC), Mastercard (#MA), Amazon (#AMZN) and Apple (#AAPL). Lastly, on Friday we get Exxon Mobil (#XOM). As for gold we note that the negative correlation of the precious metal’s price with the USD continues to be inactive as both trading instruments edged higher for the week, with gold touching new record highs. Fundamentals leading the precious metal may include a number of uncertainties on a geopolitical level, providing support for gold and we may see that course being maintained should market worries be enhanced.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.