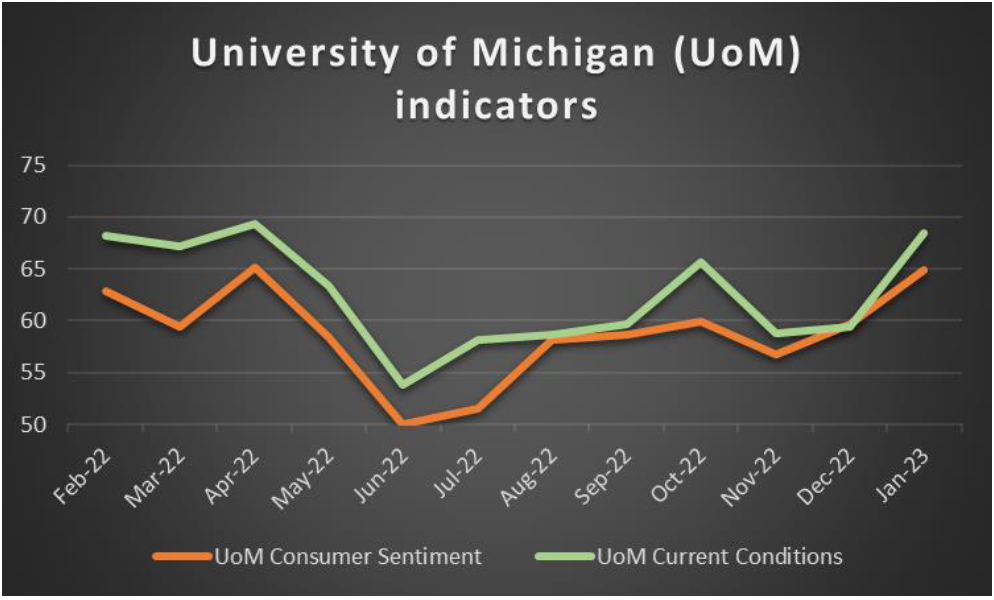

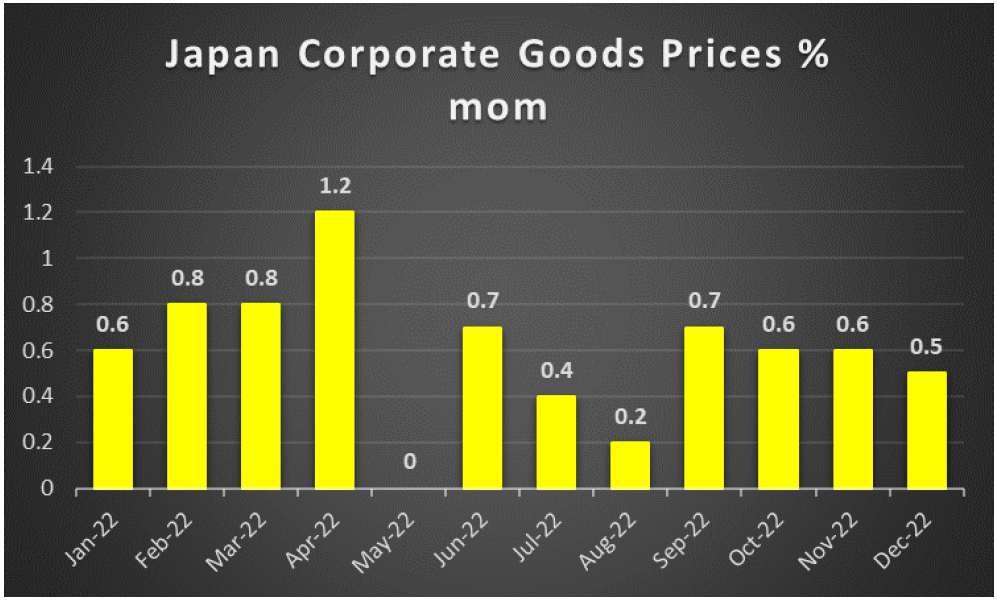

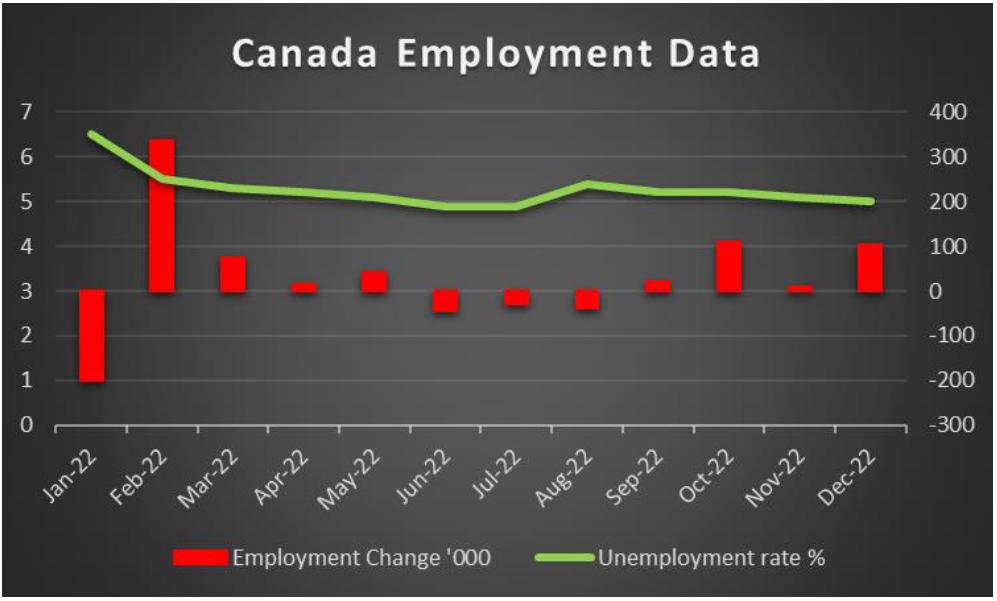

As we leave behind us a shaky week for the markets and with the US employment report for January still to be released, we open a window at what next week has in store. On the monetary front, we highlight RBA’s interest rate decision during Tuesday’s Asian session, while from Sweden we get Riksbank’s interest rate decision during Thursday’s European session. As for financial releases, we make a start on Monday with Australia’s retail trade growth rate for Q4 and continue with Germany’s industrial orders growth rate for December and preliminary HICP rate for January, while we also note Eurozone’s Sentix index for February. On Tuesday, we get Germany’s industrial output for December, UK Halifax House Prices for January and Canada’s trade data for December. On Wednesday we get Japan’s current account balance and on Thursday, we note the release of the US weekly initial jobless claims figure as well as New Zealand’s electronic card retail sales for January. Finally, on Friday, we get Japan’s corporate goods prices, China’s inflation metrics, Norway’s CPI rates and Canada’s employment data, all being for January, while from the UK we get the preliminary GDP rate for Q4 and from the US the preliminary university of Michigan consumer sentiment for February.

USD – Fundamentals to take over

The USD is about to end the week near the same levels the week began against its counterparts, yet January’s employment report with its NFP figure is still to be released and could alter the greenback’s direction. A key release that weakened the USD was the Fed’s interest rate decision on Wednesday. The bank as was widely expected proceeded with a 25-basis points rate hike cementing the downshift in its rate hiking path. Yet more rate hikes are to be expected as in its accompanying statement the bank mentioned that “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time”. On the other hand, Fed Chairman Powell sounded to be tilting towards the dovish side. The Fed Chairman characteristically stated that despite inflationary pressures easing in the US economy the bank’s battle against rising prices is far from over, and he added that “We can now say for the first time that the disinflationary process has started”. He even did not exclude the possibility of rate cuts this year should inflation come down much more quickly. Overall, the event had a bearish effect on the USD, while it provided extensive support for US stock markets. Yet should Fed policymakers come out with some hawkish comments in the coming week, we may see the market’s expectations being contradicted and USD may start losing ground. Overall, we expect in the coming week the USD to be driven mostly by fundamentals as the number of high-impact financial releases stemming from the US is to be reduced.

GBP – GDP rates eyed at the end of the week

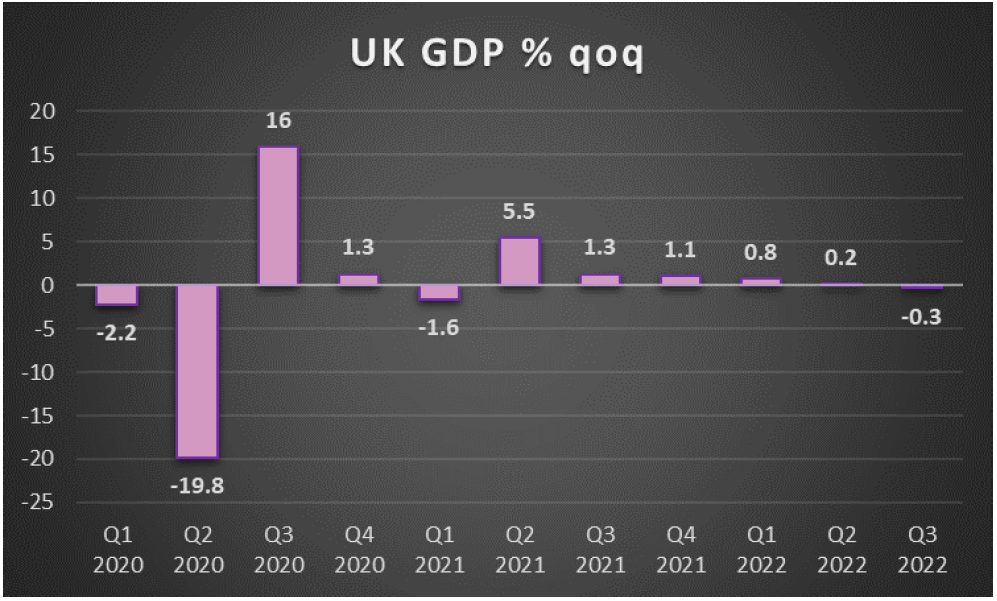

The pound is about to end the week lower against the USD, the EUR and JPY in a sign of a broader weakness. BoE’s interest rate decision on Thursday tended to provide such bearish tendencies for the pound. The bank as was widely expected hiked rates by 50 basis points raising the interest rate from 3.50% to 4.00%. The bank in its accompanying statement mentioned that “UK domestic inflationary pressures have been firmer than expected” yet also noted that “Headline CPI inflation has begun to edge back and is likely to fall sharply over the rest of the year”. It was characteristic that BoE Governor Andrew Bailey stated in his press conference following the decision that the bank sees the first signs that inflation has turned a corner. Also, BoE Governor Bailey stated that the bank will continue to monitor data very carefully, which tends to imply that there is less certainty about future rate hikes and a less hawkish approach. The decision was reached by a 7-2 majority as the two dissenting members favored for the bank to remain on hold showing that there is resistance to further rate hikes within BoE and also we note the bank’s hint that the bank rate may be nearing its peak. On a macro level, we note that the nationwide house prices growth rate showed another contraction, wider than expected, this time for January, being in the reds for four consecutive months, possibly a result also of BoE’s monetary policy tightening. Market attention next week turns towards the preliminary GDP rate for Q4 given the worries about a recession in the UK economy. Mind you that the IMF expects the UK economy to be the only major economy to shrink in 2023 and another contraction of the GDP rate on a quarter-on-quarter may not go down well with investors.

JPY – BoJ to maintain its ultra-loose monetary policy

JPY is about to end the week stronger against the USD, the EUR, and GBP and generally strengthened in the past few days. It should be noted, though that on a macro level, Tokyo’s CPI rates accelerated further for January and more than what the market expected in a sign that inflationary pressures in the Japanese economy are intensifying. On the production side of the economy, we note that the industrial production growth rate for December contracted, less than expected but still dropped, while the contraction of economic activity in the Japanese manufacturing sector was confirmed by the final PMI figure for January. So on a production level, the situation remains dire, yet there seems to be hope on the consuming side of the economy as the retail sales growth rate accelerated beyond expectations for December, which may also imply

a feeding of inflationary pressures. On a monetary level, we note that despite the tweaking of its ultra-loose monetary policy the bank seems to remain firmly dovish. It was characteristic that a Japanese panel of academics and business executives, stated that the bank would have to be more flexible, yet BoJ Deputy Governor answered promptly by stating that the bank should be more cautious in regards to any further widening of the tolerance bands around the Japanese Governments Bond’s 10-year yield, a statement that was perceived as dovish. So overall, we tend to view BoJ as remaining very dovish and keen to maintain its ultra-loose monetary policy, something that may weigh on JPY.

EUR – ECB remains hawkish yet EUR slips

The common currency seems about to end the week stronger against the USD and GBP but not the Yen. It should be noted that EUR’s strengthening against the USD came about despite ECB’s interest rate decision on Thursday weakening the common currency. It should be noted that ECB as was widely expected hiked rates by 50 basis points. In its accompanying statement, the bank in its forward guidance set the pace for the next rate hike, as it stated that “the Governing Council intends to raise interest rates by another 50 basis points at its next monetary policy meeting in March”, yet subsequent rate hikes are to be re-examined. It also reaffirmed its intentions to start quantitative tightening from next month, which could provide additional strains to Eurozone’s liquidity. Overall there seemed to be little if any hawkish surprises for the market as the bank stuck to the script of the market’s expectations, allowing for the common currency to dip against the USD, especially during Lagarde’s press conference later on. On a macroeconomic level, we note that Eurozone’s preliminary GDP rate for Q4 seems to avoid falling into the negatives, a sign that caused some analysts to mention that the area’s economy may be able to avoid a recession or suffer only a shallow one. Also, we note that the preliminary HICP rate of the Eurozone as a whole for January slowed down more than expected, reaching 8.5% yoy, in a sign that inflationary pressures seem to be easing. Yet the HICP rate remains at a relatively high level given ECB’s inflation target of 2%, which is expected to prompt the bank in more monetary policy tightening and thus further slowing, or even contraction of economic activity.

AUD – RBA’s interest decision in focus

AUD is about to end the week near the same levels it began against the USD. Aussie traders seem to be turning their attention towards RBA’s interest rate decision. The bank is expected to hike rates by 25 basis points and AUD OIS imply a probability of 79.61% for such a scenario to materialise, while the rest imply that the bank may remain on hold at 3.10%. It should be noted that the acceleration of the headline CPI rate on a year-on-year level and the relatively tight employment market despite the drop of the employment change figure into the negatives for December, adds more pressure on the bank to tighten its monetary policy. Should the bank proceed with a 25 basis points rate hike as expected, we may see the Aussie getting some support, yet market attention is expected to turn towards Governor Lowe’s accompanying statement. Should the statement maintain a clear, confident, hawkish tone, we may see AUD gaining further. Should the bank express doubts about the possible tightening of its monetary policy the rate hike may turn to a dovish hike weakening the Aussie. On a macro-economic level, besides the acceleration of inflation, we would also note that the retail sales growth rate for December, contracted more than expected, a development that sets doubts about the ability and willingness of the average Australian consumer to spend more in the Australian economy. On a more fundamental level, we note that China’s reopening may continue benefiting Australia’s economy, while the expansion of economic activity for China’s manufacturing sector could provide a boost to Australian exports of raw materials.

CAD – Employment data near the end of the week

The CAD is also about to end the week against the USD, slightly lower. It should be noted though that the drop in oil prices for the week may have prevented the Loonie from making some gains. The situation in the oil market remains relatively fluid with growing market worries for the demand side of the commodity in the past few days. The consecutive build-ups of US inventories as reported by both EIA and API as well as the drop in the number of active oil rigs, as reported by Baker Hughes, tended to highlight exactly such risks in the US oil market. Yet on the other hand, the possibility of the global economic slowdown being shallower than expected tends to improve expectations for the demand side of oil. The IMF report was characteristic to that end, citing China and India, both being large consumers of oil, as the frontrunners of economic

growth. Should oil prices continue their journey south, we may see the Loonie suffering as well, given that Canada is a major oil-producing country. On a monetary level, we note that the Canadian Government’s fiscal spending may be making the job of BoC harder, in the sense that it will have to drain more liquidity out of the Canadian economy. Yet we remind our readers of BoC’s rate hike last week, at which the bank seemed to signal a pause in the tightening of its monetary policy. On a macroeconomic level, we note the slowdown of retail sales yet not as wide as expected, while the GDP rate managed to remain in the positives, while the manufacturing PMI figure showed an expansion of economic activity for the sector, a positive for the Canadian economy. In the coming week, we expect January’s employment data to dominate Canadian financial releases, as it’s to be a key driver along with inflation for BoC’s intentions. Should January’s employment data suggest a tight employment market we may see the CAD getting some support and vice versa.

General Comment

As a closing comment, we note that the USD may allow for some of the initiative to be taken over by other currencies, given that the frequency and gravity of US financial releases tend to ease. Such a development may allow for a more balanced blend of trading opportunities for the average FX trader. Other than that, let’s not forget that the earnings season is still on, and US stock market indexes except Dow Jones seem to be in the greens. Next week fresh earnings reports are expected to keep pouring in and among them, we highlight Disney and Uber on Wednesday, as well as PepsiCo, Unilever, PayPal and Philip Morris on Thursday. Overall the market mood, is expected to continue to be affected by how well companies have performed in Q4 and may have an overspill in the FX market as well. As for Gold’s price, we highlight that the negative correlation between gold and the USD seems to have been interrupted in the current week, et we would not be surprised to see it resurfacing in the coming week.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.