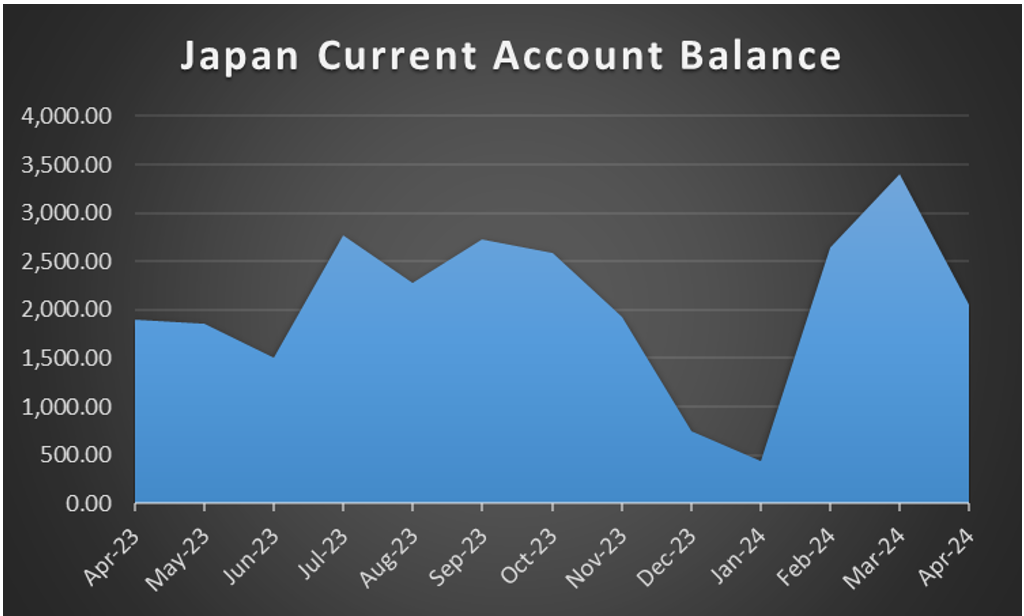

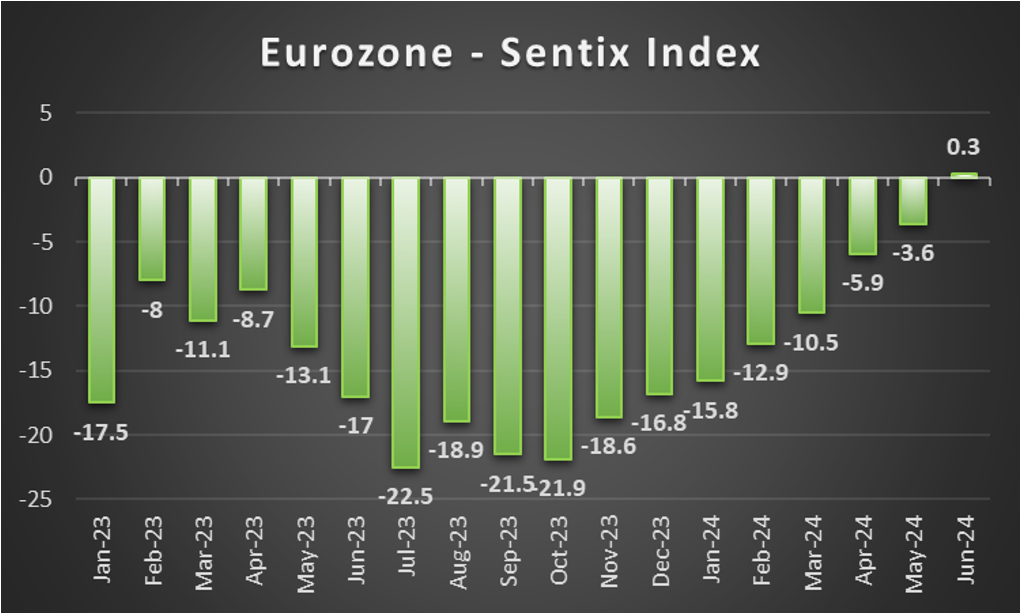

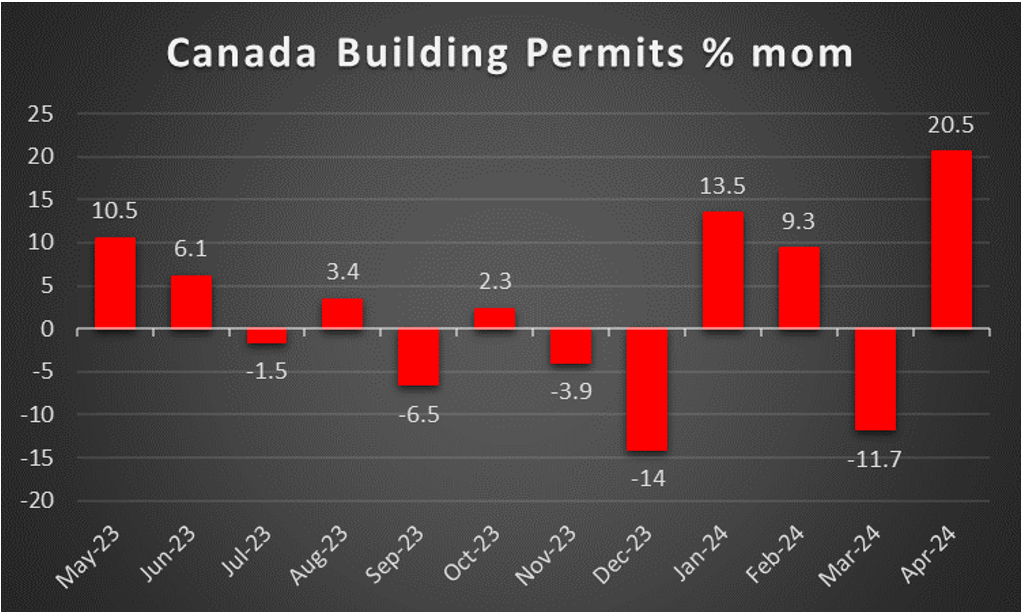

As the week draws to a close we have a look what next week has in store for the markets. On the monetary front, we note the release of New Zealand’s RBNZ interest rate decision on Wednesday, While on Tuesday, Fed Chairman Jerome Powell testifies before the US Congress. As for financial releases, we note that on Monday we get Japan’s current account balance for May and Eurozone’s Sentix index for July. After a quiet Tuesday, on Wednesday we get Japan’s corporate goods price, China’s, Norway’s and the Czech Republic’s inflation metrics all being for June. On Thursday we get Japan’s machinery orders and UK’s GDP rates both being for May, while later on we get from the US the weekly initial jobless claims figure and we highlight the release of CPI rates for June. On Friday, we get Sweden’s CPI rates for June, the US PPI rates also for June, Canadas’ building permits for May and the University of Michigan consumer sentiment for July.

USD – June’s US CPI rates in sight

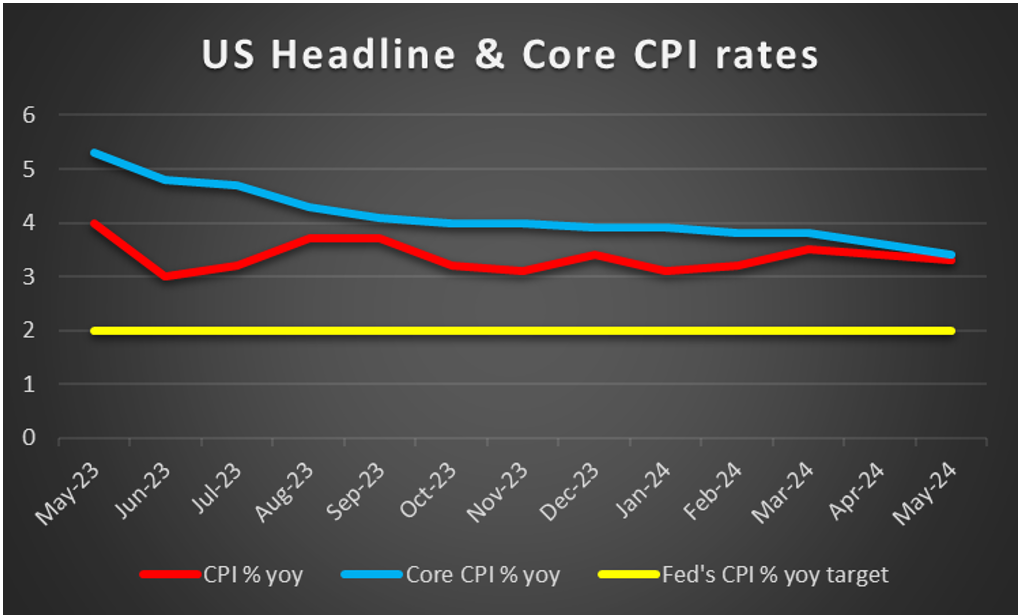

The USD retreated across the board over the course of the week, in a sign of wider weakness. On a macroeconomic level our worries for the US are intensifying given that both the ISM manufacturing and non manufacturing PMI figures implying a contraction of economic activity in the past month. Furthermore the US employment market seems to be easing, yet the US employment report for June is still to be released and could shake the markets in today’s American session. Our focus in the coming week, is to be set on the US CPI rates for the past month and a possible failure of the rates to slow down, may imply more persistent inflationary pressures in the US economy and harden the Fed’s stance to keep rates high for longer. Thus such a scenario could provide some support for the USD. Monetary policy wise, we note that the release of the Fed’s June meeting minutes revealed relatively little new, and in the coming week we intend to concentrate more on Fed Chairman Powell’s testimony before Congress. Should the Fed’s Chairman show further hesitation to start cutting rates we may see the USD gaining some ground and vice versa. On a fundamental level, we note that the scenery of the US Presidential elections remains somewhat blurry on the Democrats side after the weak performance of US President Biden on the debate. It should be noted that the pressure to change the Democratic candidate is increasing as time progresses and the perception that US Presidnet Biden may be too weak to win Trump seems to be gaining ground among Democrats.

GBP – UK GDP rates due out

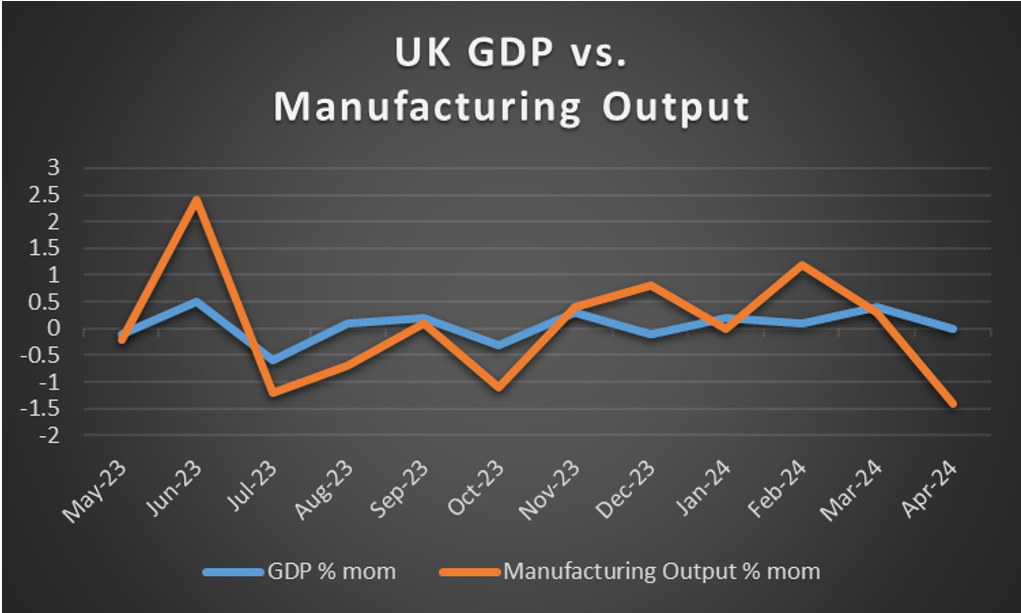

the pound is about to end the week higher against the USD, the JPY and the EUR in a sign of wider strength. On a fundamental level for pound traders, we note that the UK general elections are now over and despite the fact that the final results have not been released yet, Labour is leading securing a comfortable majority in the UK Parliament. The pound seems to have gotten some additional support, as the wide majority of the Labour party, seems to provide a relative stability in the UK political outlook. The change in government is exected to alter the fiscal path of the UK, probably widen fiscal spending and could affect the course of the sterling. On a monetary policy level, we note the market’s expectations for a rate cut in the BoE’s next meeting and another one in the December meeting. The market’s expectations may be exercising some downward pressure on the pound for the time being. The current restrictive interest rate level, is expected to provide more pain in the coming months to mortgage owners and could have an adverse effect on economic activity and the labour market in the UK. On a macroeconomic level, we note that House prices have risen, in a positive sign of increased demand in the UK real estate sector. As for economic activity we note some mixed signals, as the PMI figure of June for the manufacturing sector came in lower than in the preliminary release, while for the services sector its sister indicator came in higher. In the coming week we intend to focus on the release of May’s GDP rates and a possible acceleration could brighten the UK economic outlook and provide some support for the sterling.

JPY – JPY at dangerously weak levels

JPY remained relatively unchanged against the USD and is about to end the week weaker against the pound and EUR. JPY remains at relatively low levels against the USD despite a slight correction in the past days and its characteristic that on Wednesday, despite USD retreating across the board, it failed to materially fall against the Yen. Main factor behind JPY’s weakness remains the interest rate outlook differentials of BoJ , given BoJ’s loose monetary policy. It’s characteristic of Japan’s worries about the issue, that Japanese Finance Minister Suzuki, reaffirmed the government’s vigilance about the FX market on Tuesday. Yet Mr. Suzuki refrained from issuing a warning about a possible market intervention. We note that as long as JPY continues to weaken, the chances of the Japanese government actually intervening in the FX markets to the Yen’s rescue, rises. Yet on the other hand, a possible market intervention may bring only temporary relief for the Yen as the fundamentals underpinning JPY’s weakness remain intact. On a macroeconomic level, we note that the Tankan big manufacturers index for Q2, rose beyond market expectations in a positive sign for economic activity in the sector. The macroeconomic hopes where somewhat clipped though as the Tankan non manufacturers index for the same quarter, edged lower. Last but not least, on a fundamental level, we note JPYs’ ability to attract safe haven inflows in times of crisis, a characteristic that could come into play next week, should tensions start escalating.

EUR – Fundamentals to lead

The common currency is about to end the week higher against the USD and the pound yet is still gaining against the JPY. EUR traders’ expectations for the bank to proceed with two rate cuts within the year seem to intensify. It’s characteristic that ECB policymaker Stournaras stated that the expectations for two more rate cuts in 2024 seem reasonable. It should be noted though that ECB President Lagarde seemed a bit uneasy with interest rate cutting, citing stubborn inflation in the services sector. Yet overall the consensus is for the bank to reduce the refinancing rate to 3.75% by the end of the year, which in turn may weigh on the EUR should market expectations intensify. On a fundamental level, we highlight the second round of the French Legislative elections and market worries for a possible win of Marine Le Pen’s far right National Rally (NR) are intense. Should NR win the elections, we may see the common currency suffering some outflows on Monday as a possible win of Le Pen could intensify centrifuge forces within the EU. On a macroeconomic level, we note the easing in inflationary pressures in the Eurozone for June as reported by the preliminary HICP rate, while some worries surface after an unexpected contraction of Germany’s industrial orders growth rate for May. Overall we view the economic recovery of the Eurozone as a bumpy road ahead and a soft landing may not be in the cards for the Zone.

AUD – Market sentiment to provide direction

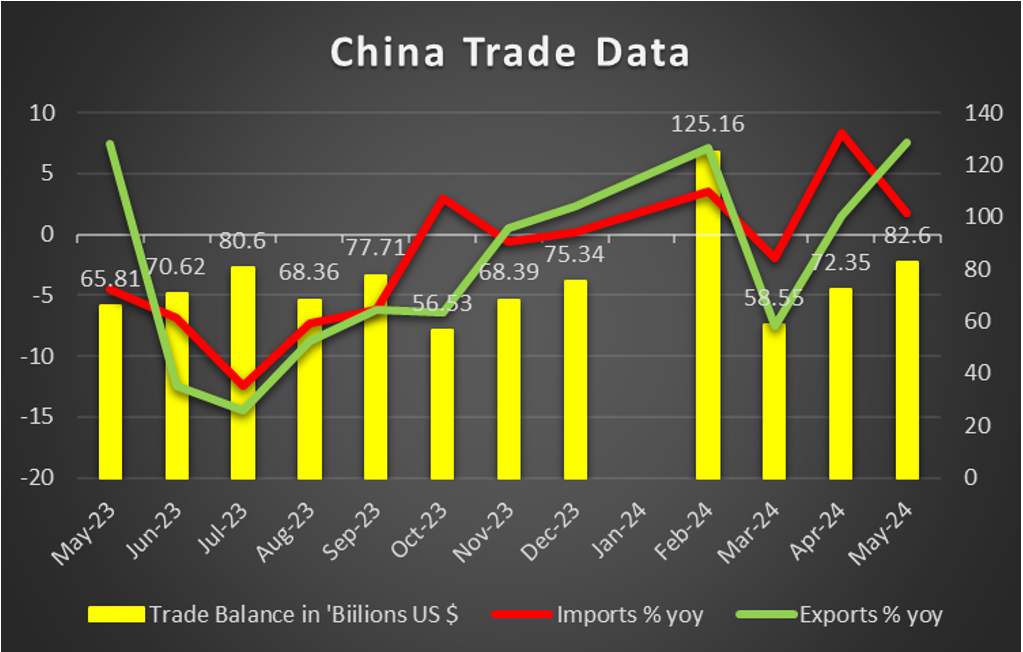

AUD is about to end the week stronger that the greenback. Aussie traders where encouraged on a mopnetary policy level after the release of the RBA’s last meeting minutes. The document revealed that the bank seemed to consider the possibility of a rate hike as it mentioned that the “board judged the case for holding rates steady stronger than for hiking”. Hence we expect that RBA’s firm stance could provide some support for the Aussie on a monetary policy level, as RBA is still considering hiking in contrast to other central banks which are considering when to cut rates. On a macroeconomic level, we note the acceleration of the building approvals and retail saels growth rates, both for May, in a sign that Australian’s have the ability and willingness to proceed with log term invenstments as well as wider consumption. In the coming week we expect it to be a bit more quiet as no high impact financial releases are expected from Australia, hence fundamentals may lead the Aussie. On a deeper fundamental level, we note that the Aussie remains highly senstive to the market sentiment as it is regarded as a risikier asset, hence an improvement of the market sentiment could provide support for the Aussie and vice versa. Also given the close Sino-Australian economic ties, we may see Chinese financial releases, especially China’s June trade data in the coming week affecting the Aussie somewhat. A possible acceleration of Chinas’ import growth rate could provide some support for the Aussie as it could imply more exports of Australian rawe material to China.

CAD – Oil prices to affect the Loonie

We note that Looney traders’ expectations for a rate cut in BoC’s July meeting seem to have eased somewhat, as a rate cut is now expected in the September meeting. Overall we tend to see the case for the bank to wait until the dust settles before making its next move. On a macroeconomic level, we note that Canada’s ermployment data for June are still to be released later today and could shake the Looney. Since our last weekly outlook we note that Canada’s GDP rate for April was released showing that the economy grew at a faster pace than expected, which tends to brighten the economic outlook of Canada somewhat. On the flip side, Canada’s trade deficit widened beyond market expectations, highlighting the outflow of wealth from the Canadian economy, due to its international trading activities. Oil prices on the other hand, seem to continue to rise given also the relative tightness of the US oil market currently and increased oil demand expectations for the summer, which in turn may be providing some support for the Looney as well, given Canada’s status as a major oil producing economy.

General Comment

Overall in the coming week, in the FX market, we expect the US to maintain the initiative over other currencies as the frequency and gravity of US events and financial data to be released is increased. Still some currencies are expected to take their own course at certain points during the week, which in turn may create a nice mix of trading opportunities. As for US stock markets, we note that all three major US stockmarket indexes, that would be NASDAQ ,S&P 500 and Dow Jones 30, were on the rise for the week in a signal of increased confidence and optimism. We tend to highlight once again that fundametnals in the US economy may not be supporting such rises currently and if actually so could force US stockmarkets to a correction lower. As for gold, we note that the negative correlation of gold prices to the USD seems to have resumed maybe assymetrically to gold’s favor. It should be noted that despite the initial rise of US yields earlier on in the week, the gains appear to have been erased at the time of this report and US bond yields are at lower levels than last Friday, which in turn may have polished the shiny metal’s appeal as well.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.